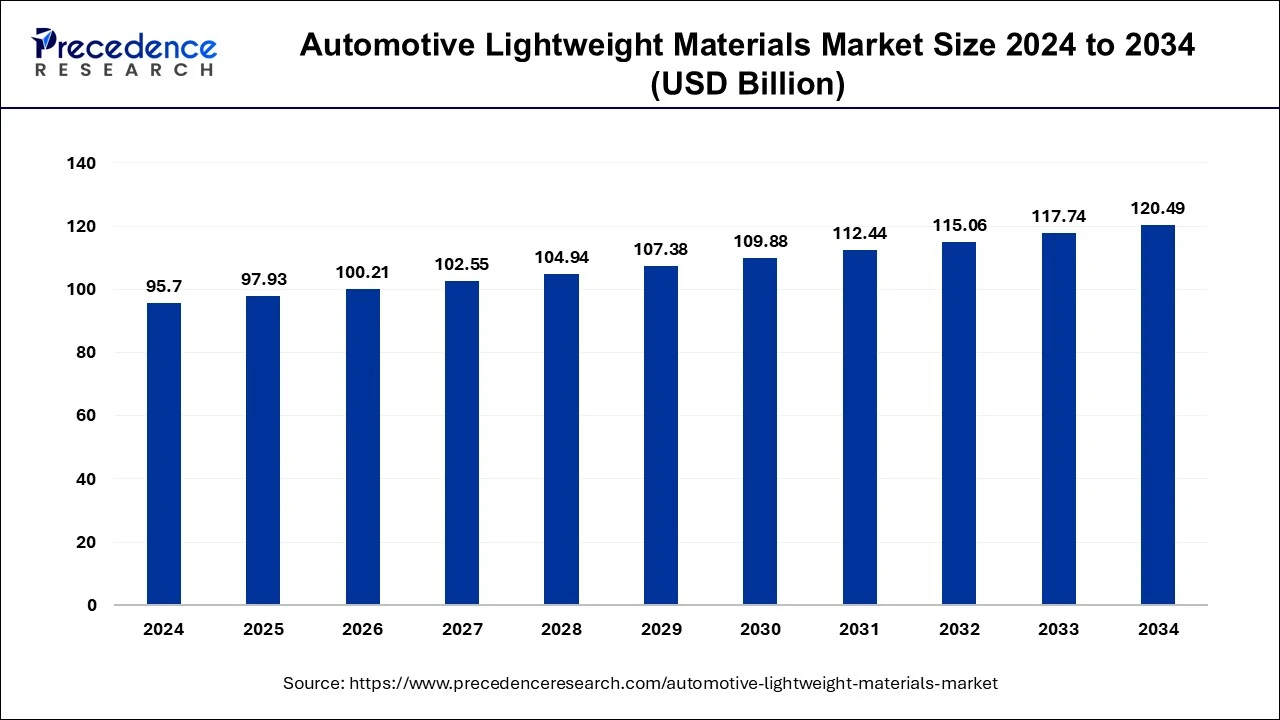

According to Precedence Research, the global automotive lightweight materials market size is expected to reach around USD 120.49 billion by 2034 from USD 95.7 billion in 2024 with a CAGR of 2.33%.

Automotive Lightweight Materials Market Key Points

- Europe led the global automotive lightweight materials market, capturing the largest share of 36.52% in 2024.

- Germany is emerging as a key contributor, witnessing a significant CAGR of 6.99% throughout the forecast period.

- North America is also projected to register healthy growth, expanding at a CAGR of 4.96% during the same period.

- Among materials, the composites segment dominated the market with a substantial 66% share in 2024.

- The plastics segment is anticipated to grow steadily, recording a CAGR of 3.83% over the forecast years.

- Based on application, Body-in-White (BiW) held the highest market share at 26% in 2024.

- The closures segment is forecasted to grow at a moderate CAGR of 2.6% during the assessment period.

- In terms of end use, passenger cars accounted for the lion’s share of the market with 83% in 2024.

- The light commercial vehicles (LCVs) segment is set to expand at a CAGR of 3.3% during the forecast timeframe.

What is the Role of AI in the Automotive Lightweight Materials Market?

Artificial Intelligence (AI) plays a critical role in accelerating innovation within the automotive lightweight materials market. AI-powered tools aid researchers in designing advanced materials by analysing vast datasets to identify optimal material compositions and structural properties. Through predictive modelling and simulations, AI helps engineers forecast how lightweight materials such as composites and alloys will perform under various real-world conditions, significantly reducing the need for physical prototyping and cutting development time and costs.

On the manufacturing side, AI enhances precision and efficiency in the production of lightweight components. Smart algorithms are used for process optimization, real-time defect detection, and predictive maintenance of equipment. This results in better material utilization, reduced waste, and higher quality control standards. AI also supports the development of more sustainable and customizable manufacturing practices, ultimately enabling automakers to meet regulatory standards and consumer demand for fuel-efficient, high-performance vehicles.

What are Automotive Lightweight Materials?

Automotive lightweight materials refer to advanced materials used to reduce the overall weight of vehicles while maintaining or improving performance, safety, and fuel efficiency. These materials include aluminum, magnesium, high-strength steel, plastics, and composites like carbon fiber and glass fiber-reinforced polymers. By replacing traditional heavy steel components, these materials help automakers achieve stricter fuel economy and emissions standards without compromising structural integrity.

Why are They Important?

Reducing vehicle weight is a key strategy to improve fuel efficiency and lower carbon emissions. Lightweight materials contribute to better acceleration, braking, and handling while also supporting the integration of electric vehicle (EV) batteries by offsetting their weight. Additionally, they enable innovative design and improve overall vehicle performance. With the automotive industry rapidly shifting toward EVs and sustainability, the demand for lightweight materials is expected to grow significantly in the coming years.

Regional Outlook of Automotive Lightweight Materials Market

Europe holds the largest market share globally, accounting for 36.52% in 2024. The region’s dominance is attributed to strict EU regulations targeting carbon emission reductions, compelling automakers to integrate lightweight materials like carbon fiber-reinforced polymers and aluminum. Germany, in particular, is at the forefront of adopting these advanced materials. The regulatory landscape and ongoing innovation in material science are expected to drive steady market growth in Europe through the forecast period

Asia Pacific leads the automotive lightweight materials market in terms of consumption, driven by the rapid adoption of electric and hybrid vehicles. Countries such as China, India, Japan, and South Korea are making significant investments to transform their public transportation sectors with advanced vehicles. These nations have also implemented stringent emission norms to address rising carbon emissions, pushing manufacturers to adopt lightweight materials that improve fuel efficiency and lower emissions. The region’s focus on sustainable mobility and regulatory pressure is expected to sustain high demand for lightweight materials

North America is experiencing growth in the automotive lightweight materials market due to increasing consumer demand for fuel-efficient vehicles and the rising popularity of electric vehicles. Regulatory initiatives to curb emissions, coupled with investments in research and development, are encouraging manufacturers to use lightweight materials in both passenger and commercial vehicles. The region’s automotive industry is also characterized by significant partnerships and technological advancements aimed at optimizing vehicle performance and efficiency

Segmental Insights of Automotive Lightweight Materials Market

Vehicle Type Insights

The passenger cars segment dominates the automotive lightweight materials market, accounting for 83% of the market share in 2024. This dominance is driven by rising consumer demand for fuel-efficient and environmentally friendly vehicles, particularly electric and hybrid models. Manufacturers are focusing on lightweight solutions to enhance battery life and range, aligning with shifting consumer preferences and stricter regulatory requirements.

The light commercial vehicles (LCVs) segment is also expanding, with a CAGR of 3.3% projected during the forecast period, as sustainability becomes a priority in commercial transport.

Material Insights

The composites segment leads the market, contributing 66% of the market share in 2024. Composites are favored for their lightweight, durable, and easily moldable properties, making them ideal for electric vehicle manufacturing.

The plastics segment is expected to grow at a CAGR of 3.83%, propelled by global regulations mandating reduced vehicle weight to improve fuel efficiency. Plastics are increasingly used in interiors, body panels, and under-the-hood applications, helping manufacturers meet performance and compliance targets.

Application Insights

The body in white (BiW) segment which includes the vehicle’s structural frame—holds the highest application share at 26% in 2024. This segment is crucial for overall vehicle weight management.

The closures segment (doors, hoods, etc.) is projected to grow at a CAGR of 2.6%, as integrating lightweight materials like aluminum, high-strength steel, and composites in these areas further reduces vehicle weight and boosts efficiency

Automotive Lightweight Materials Market Scope

- Market Size in 2024: USD 95.70 Billion

- Market Size in 2025: USD 97.93 Billion

- Market Size by 2034: USD 120.49 Billion

- Growth Rate (2025–2034): CAGR of 2.33%

- Segments Covered: Vehicle, Material, Application, Region

Automotive Lightweight Materials Market Companies

- Henkel AG & Co.

- DuPont

- NovaCentrix

- KGaA

- Intrinsiq Materials, Inc.

- Creative Materials Inc.

- Vorbeck Materials Corporation, Inc

- Johnson Matthey PLC

- Heraeus Holding GmbH

- Applied Ink Solutions

combined with superior switching performance")

{kind=link}