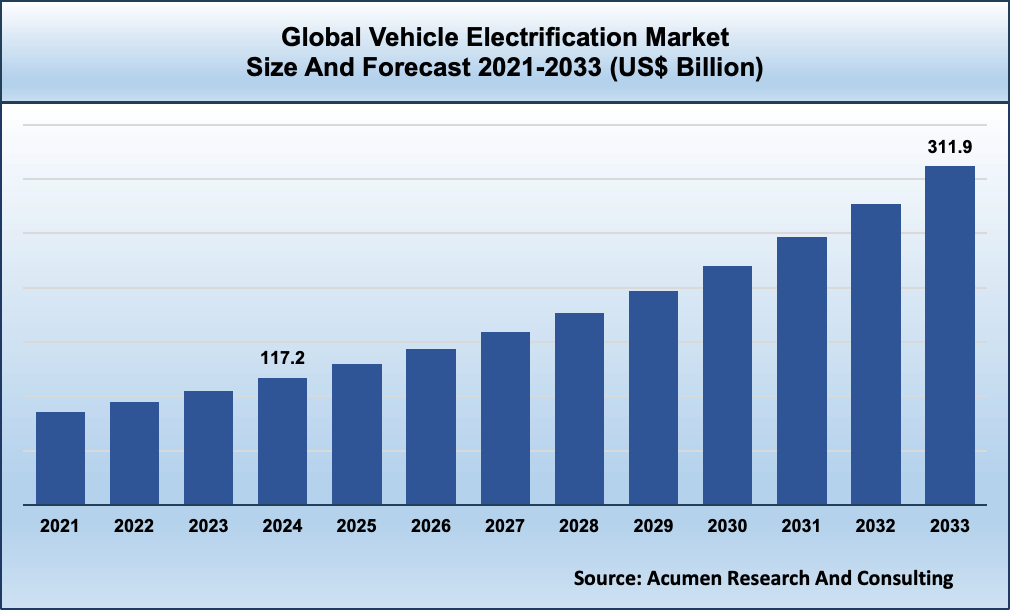

According to recent data from Acumen Research and Consulting, the global Vehicle Electrification Market Size reached approximately USD 117.2 billion in 2024 and is projected to exceed USD 311.9 billion by 2033, expanding at a compound annual growth rate (CAGR) of 11.6% during the forecast period. This growth trajectory reflects the mounting influence of regulatory pressures, consumer preference for cleaner mobility, and rapid advancements in battery and powertrain technologies.

As the global transportation landscape shifts toward sustainability, the vehicle electrification market is emerging as a key catalyst in the mobility revolution. Once considered a niche segment, electrification technologies have now become foundational to the future of the automotive industry—transforming not only passenger vehicles but also two-wheelers, commercial fleets, and public transport.

What is Vehicle Electrification?

Vehicle electrification refers to the integration of electric power into the various vehicle systems traditionally powered by mechanical or hydraulic energy. This includes components such as power steering, air conditioning, braking, and drivetrain systems. Electrification goes beyond electric vehicles (EVs); it also involves micro-hybrids, mild hybrids, plug-in hybrids, and fuel cell vehicles—each representing varying levels of electrification.

Vehicle Electrification Market Overview: Key Statistics

- Market Size in 2024: USD 117.2 Billion

- Estimated Market Size by 2033: USD 311.9 Billion

- CAGR (2025–2033): 11.6%

- Leading Segments: ICE Electrification, Hybrid and Battery Electric Vehicles

- Key Regions: North America, Europe, Asia-Pacific

Core Drivers of Vehicle Electrification Market Growth

- Regulatory Pressure and Global Emission Standards

Tightening emission standards across the globe are placing significant pressure on OEMs to reduce CO₂ emissions. In Europe, regulations like the EU Green Deal are pushing manufacturers toward zero-emission fleets. Similarly, the U.S. and China are offering generous subsidies and fuel economy mandates to accelerate electric adoption.

- Surging EV Sales and Infrastructure Expansion

The meteoric rise of battery electric vehicles (BEVs) and plug-in hybrid vehicles (PHEVs) is a strong contributor to vehicle electrification market growth. Global EV sales crossed 10 million units in 2023, and with charging infrastructure scaling rapidly, electrification is becoming more viable than ever.

- Integration of Advanced Technologies

Modern electrified systems now feature AI-powered battery management, regenerative braking, and digitally controlled e-axles. Innovations in wide-bandgap semiconductors (SiC, GaN) are also enhancing inverter and converter performance, supporting long-term vehicle electrification market trends.

- Demand for Lightweight and Efficient Components

Electrification supports the move toward lighter and more compact components, improving vehicle efficiency. As OEMs focus on reducing overall energy consumption, electrification of auxiliary systems such as HVAC and suspension becomes increasingly essential.

Vehicle Electrification Market Regional Landscape: Asia-Pacific Dominates, North America Accelerates

Asia-Pacific holds the largest vehicle electrification market share, with China leading the charge due to aggressive EV mandates, local manufacturing dominance, and battery technology leadership. Japan and South Korea continue to invest heavily in hydrogen fuel cell vehicle (FCV) development and high-efficiency hybrid powertrains.

North America is witnessing accelerated adoption, thanks to federal EV incentives, Tesla’s market leadership, and new entrants like Rivian and Lucid Motors. The Inflation Reduction Act (IRA) is also acting as a tailwind for EV and EV component manufacturing across the U.S.

Europe remains a tech and policy leader in sustainability and electrification, with major automakers committing to full-electric lineups by 2030. The region is also home to battery gigafactories and green hydrogen pilot programs that align with electrification goals.

Industry Trends Transforming the Market

Electrification of Commercial Vehicles

Fleet operators are transitioning to electric delivery vans, trucks, and buses. Electrification improves operational efficiency and lowers total cost of ownership (TCO). Companies like Volvo, BYD, and Daimler are scaling commercial EV offerings, boosting demand for power modules and battery packs.

EV + AI: Smart Electrification

The convergence of artificial intelligence and electrification is enabling smart routing, predictive maintenance, and optimized battery charging. AI-integrated energy management systems are increasingly embedded into EVs to monitor and adapt to real-world driving behavior.

Vehicle-to-Grid (V2G) Integration

As EVs double as energy storage units, V2G capabilities are becoming a key value proposition. This model allows bidirectional energy flow between the EV and the grid, promoting sustainability and grid resilience.

Battery Chemistry Innovations

Solid-state batteries, lithium-sulfur, and LFP (lithium iron phosphate) chemistries are improving energy density, reducing costs, and enhancing safety—core pillars of vehicle electrification market growth.

Challenges and Roadblocks in the Vehicle Electrification Market

Despite the strong momentum behind the vehicle electrification market, the transition from internal combustion engine (ICE) vehicles to electrified mobility faces several complex challenges that could slow its adoption curve if not addressed collaboratively across industry and policy ecosystems.

Infrastructure Gaps and Charging Accessibility

One of the most pressing challenges in the vehicle electrification landscape is the limited availability of EV charging infrastructure, especially in rural and emerging markets. While urban centers are seeing an uptick in fast-charging stations, the gap between EV demand and infrastructure readiness is significant. Range anxiety continues to be a concern for consumers, particularly those living in apartment complexes or areas without home-charging options.

Public-private partnerships are necessary to build a robust, interoperable charging network that supports high-speed DC chargers and integrates renewable energy sources. Additionally, standardization of charging protocols (CCS, CHAdeMO, etc.) remains inconsistent across geographies, affecting user experience and scalability.

Battery Material Supply Chain Risks

The surge in demand for lithium-ion batteries has spotlighted vulnerabilities in the raw materials supply chain, particularly for lithium, cobalt, and nickel. Many of these materials are sourced from geopolitically sensitive regions, raising concerns over supply stability, ethical mining practices, and environmental degradation.

As automakers and governments push for local sourcing and battery recycling initiatives, the market must adapt by investing in alternative chemistries (such as LFP and solid-state) and enhancing battery lifecycle management. Without intervention, bottlenecks in material availability could constrain vehicle electrification market growth in the medium term.

High Upfront Costs and TCO Education

Electrified vehicles still carry a higher upfront price tag than their ICE counterparts, primarily due to the cost of battery packs and advanced electronics. While the total cost of ownership (TCO) often favors EVs over time—thanks to lower fuel and maintenance costs—consumer perception still tends to focus on purchase price.

Many potential buyers remain unaware of available incentives, rebates, and long-term savings, indicating a need for stronger consumer education campaigns. Bridging this knowledge gap is crucial for achieving mass adoption and increasing vehicle electrification market share globally.

Serviceability and Aftermarket Limitations

Unlike traditional vehicles, electrified systems require specialized maintenance and diagnostics. The current automotive aftermarket ecosystem is largely unprepared to support complex EV systems like high-voltage batteries and electric drivetrains. This presents a challenge for independent repair shops and raises questions about vehicle downtime, cost of parts, and technician training.

OEMs, service networks, and vocational institutions must invest in EV technician certification programs and diagnostic tooling to ensure the ecosystem is ready to support the coming wave of electric vehicles.

Manufacturing Transition and Workforce Readiness

As automakers pivot toward electrified platforms, legacy manufacturing lines must undergo significant retooling. This includes new supply chain management systems, automation upgrades, and digital integration across production cycles. Equally important is workforce reskilling—many traditional automotive roles are being replaced or redefined in this new electrification era.

This structural shift demands capital expenditure, retraining programs, and regulatory alignment—especially for suppliers and small- to mid-sized Tier 2 and Tier 3 vendors that may not have the resources to adapt quickly.

Outlook: What’s Ahead for the Vehicle Electrification Market?

The vehicle electrification market outlook to 2032 suggests a steep rise in technological adoption, cross-sector partnerships, and supply chain localization. OEMs, Tier 1 suppliers, and governments must coordinate efforts to create a resilient and scalable electrification ecosystem.

The future will likely include:

- A stronger push toward software-defined vehicles

- Broader deployment of bidirectional charging solutions

- Circular battery economies supporting sustainability

- A shift from component-level to system-level electrification strategies

The vehicle electrification market is more than a trend—it’s a systemic transformation of mobility, energy, and technology. With innovation surging in every direction—from silicon chips to smart drivetrains—the market is set to redefine how vehicles are built, powered, and connected.

By 2033, electrification will be at the heart of nearly every transportation solution, enabling cleaner air, smarter cities, and energy-efficient lifestyles.

combined with superior switching performance")

{kind=link}