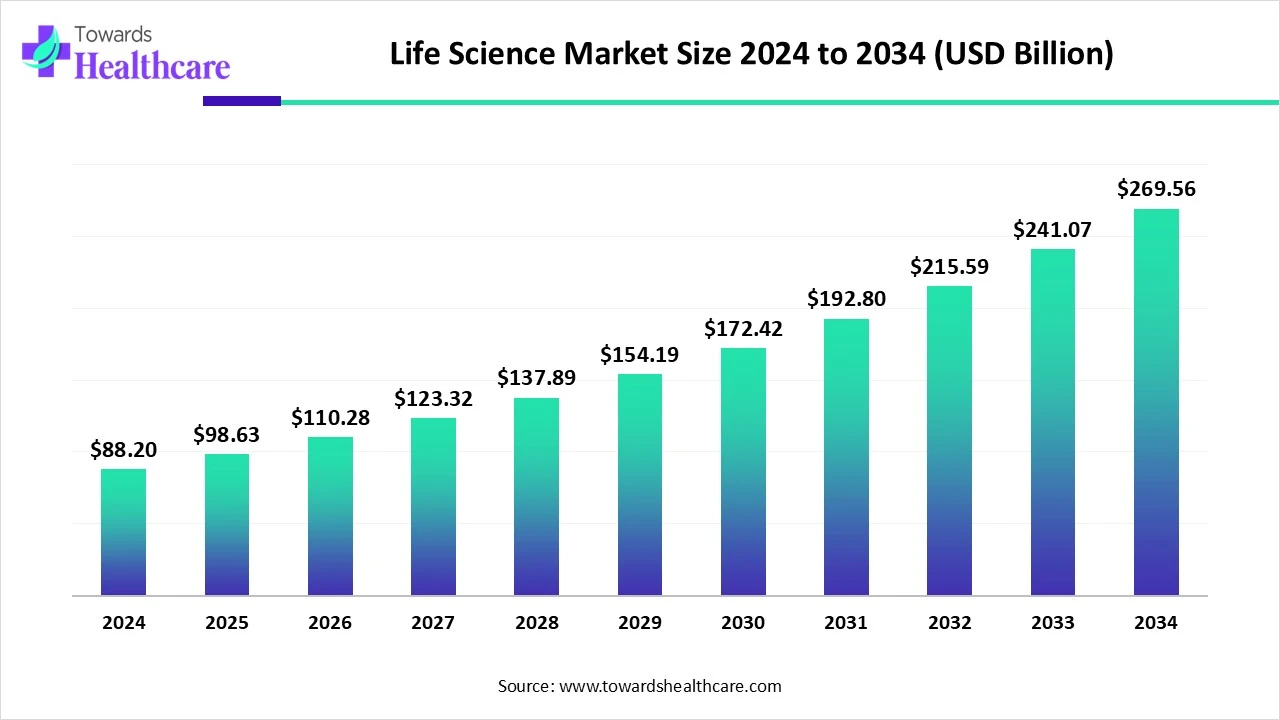

As the 21st century unfolds, few sectors have shown as much transformative promise and dynamic growth as the life sciences. From biotechnology breakthroughs to AI-enabled drug discovery, the global life science market is rewriting the rules of healthcare, diagnostics, and medical innovation. According to market projections, the industry is set to grow from USD 88.2 billion in 2024 to a staggering USD 269.56 billion by 2034, driven by a robust CAGR of 11.82%. This momentum reflects not only scientific advancement but also a strategic confluence of investment, government support, and technological disruption.

The Lifeblood of Life Sciences: Research, Discovery, and Personalized Solutions

At the heart of this transformation is research and development (R&D). Whether it’s decoding the human genome or engineering targeted therapies, R&D is enabling scientists to create medicines and devices tailored to individual patient needs. As chronic diseases rise globally, the demand for personalized medicines, advanced diagnostics, and high-performance therapeutics continues to surge.

Genetic profiling, for instance, is reshaping how we approach treatment moving beyond the “one-size-fits-all” approach to therapies that treat diseases at their root. Meanwhile, biologics and biosimilars are finding favor over traditional drugs, offering precision in treatment with fewer systemic side effects.

Market Leaders and Regional Outlook

North America: Innovation Powerhouse

The U.S. leads the global life science market, supported by strong infrastructure, academic research, and regulatory momentum. In 2024 alone, the FDA approved 50 new drugs, and the National Institutes of Health (NIH) committed over $48 billion toward medical research. With over 45,000 life science companies operating in the country, the U.S. continues to be a hub for new drug development, digital health platforms, and advanced manufacturing.

Canada, too, is making notable strides. It boasts more than 2,000 life science firms, and between 2019 and 2023, investments in its biotech sector reached nearly $26 billion. The Canadian government remains committed to supporting life science innovation, pledging more than $308 million in 2024 alone.

Asia-Pacific: The Next Frontier

Asia-Pacific is the fastest-growing region in this sector, with China and India at the forefront. China’s booming startup ecosystem, particularly in Beijing and Shanghai, and a 379% surge in patent filings from 2014 highlight its aggressive push into life sciences. India, meanwhile, is becoming a biotech powerhouse with over 8,500 startups and substantial venture capital backing estimated at $13.7 billion in 2024, making it the second-largest VC destination in the region.

Europe: A Steady Pillar

Europe’s life science growth is supported by strong governmental frameworks and favorable trade policies. Countries like Germany and the UK are among the top exporters of pharmaceutical products, and European Commission initiatives are laying the foundation for future R&D growth. Germany’s new “Digital Health” strategy and the UK’s £520 million commitment to innovative manufacturing further strengthen the region’s position.

Latin America, MEA: Emerging Potential

Latin America, particularly Brazil, is emerging as a regional leader in clinical trials and biotech innovation. In Africa and the Middle East, increasing government funding, digital adoption, and rising clinical trial activity point toward promising growth. MEA countries allocated over $10 billion to life science R&D, with M&A activity surging in late 2024.

Key Market Segments: What’s Driving Growth?

Pharmaceuticals Lead the Charge

The pharmaceuticals segment dominated the market in 2024, fueled by the rise of generic drugs and novel drug development. Small molecule drugs continue to be popular due to their cost-effectiveness and accessibility. The increasing annual R&D spending by contract research and development organizations, which grew by 12–13% from 2014 to 2022, is another crucial driver.

Biotechnology is expected to grow at the fastest CAGR in the coming decade, driven by advances in genomics, proteomics, and biologics. Meanwhile, the medical devices segment is benefiting from the growing use of wearables and AI-enabled diagnostic tools.

Therapeutics and Drug Development Dominate Applications

The therapeutic application segment held the largest market share in 2024, thanks to a rising need for targeted and recombinant therapies. But the spotlight is now shifting toward drug discovery and development, which is expected to register the fastest growth. As of mid-2025, over 540,000 clinical trials were registered globally a testament to the sector’s rapid expansion and rigorous research standards.

Diagnostics, too, is gaining ground, with governments launching screening initiatives and promoting routine health checks. More than 50% of adult cancer diagnoses now occur during routine exams, underscoring the importance of proactive diagnostics.

Oncology: A Critical Therapeutic Area

Cancer remains the leading therapeutic focus within the life sciences industry. By 2050, global cancer cases are expected to hit 35 million, driving demand for innovative treatments. In 2023 alone, 25 new oncology drugs were introduced, and over 2,000 clinical trials focused on cancer therapies were launched.

Infectious diseases and cardiology follow closely, especially in developing regions where healthcare systems are racing to catch up with rising disease prevalence.

AI and Digital Health: The Next Big Wave

Artificial Intelligence is becoming deeply embedded across the life science value chain from research and development to clinical trials, manufacturing, and supply chain logistics. AI-enabled platforms now help identify drug targets, automate regulatory compliance, and personalize patient care.

Wearable technologies and healthcare apps are also redefining patient engagement. More than 320 million people used health-related applications globally in 2024, and the use of smartwatches and health bands continues to rise.

Noteworthy Industry Developments

- Honeywell launched TrackWise Manufacturing, an AI-powered workflow management platform to boost efficiency in life science production.

- Clarivate plc introduced DRG Fusion, a platform designed to enhance commercial analytics in pharma and medtech.

- Accenture invested in 1910 Genetics to accelerate AI-driven drug discovery.

- Axtria, a key player in GenAI-driven analytics, continues to empower life science companies through data-led transformations.

Challenges and Opportunities Ahead

While the outlook is overwhelmingly positive, the life sciences sector is not without its hurdles. Regulatory compliance remains a persistent challenge, especially with evolving laws around clinical trials and drug approvals. Cybersecurity and data privacy also pose concerns as companies digitize operations.

However, the sector’s resilience is evident in how it has embraced genetic engineering, AI, and telemedicine. Technologies like CRISPR are revolutionizing treatment strategies for genetic and rare diseases, while growing digital adoption is enhancing access and efficiency in healthcare delivery.

combined with superior switching performance")

{kind=link}