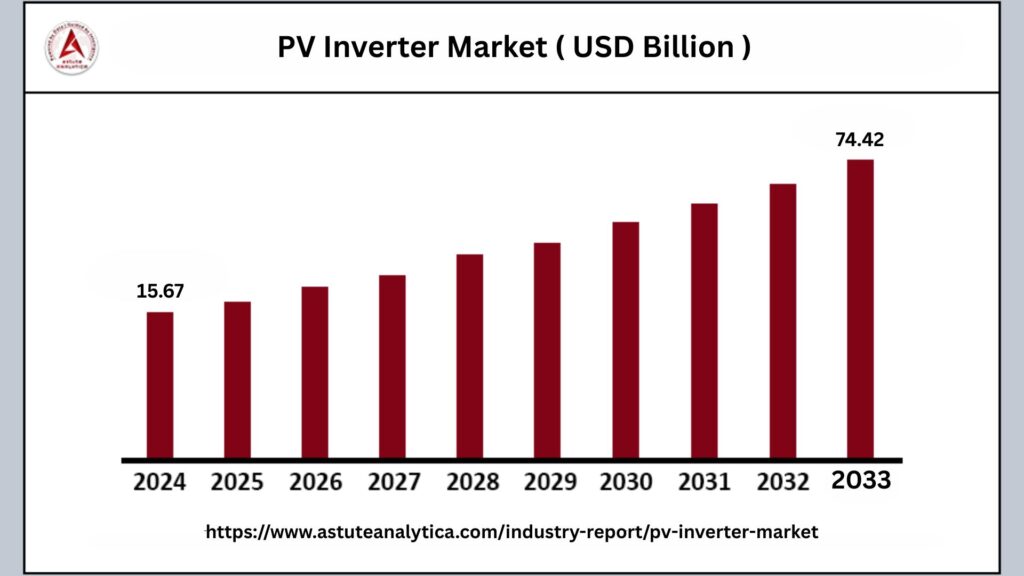

The global PV inverter market was valued at US$ 15.67 billion in 2024 and is projected to reach US$ 74.42 billion by 2033, reflecting a Compound Annual Growth Rate (CAGR) of 18.9% during the forecast period from 2025 to 2033.

A Photovoltaic (PV) inverter, commonly known as a solar inverter, plays a crucial role in solar energy systems by converting the direct current (DC) electricity generated by solar panels into alternating current (AC) electricity. This conversion is essential because AC electricity is the standard form of power used by household appliances, commercial operations, and the broader electrical grid.

The global PV inverter market is currently undergoing a phase of remarkable expansion and transformation. This growth is fueled by an escalating worldwide demand for renewable energy solutions as governments, industries, and consumers look to reduce carbon emissions and transition to sustainable power sources. As a result, shipment volumes of PV inverters have reached record highs, reflecting the rapid deployment of solar installations across residential, commercial, and utility-scale sectors.

PV Inverter Market Key Takeaways

- By type, string PV inverters hold a significant position in the global PV inverter market, commanding over 48% of the market share.

- By end use, utility-scale applications dominate the PV inverter market globally, accounting for over 57% of the market share.

Regional Analysis

Dominance of the Asia-Pacific Region in the PV Inverter Market

The Asia-Pacific region holds an overwhelming command over the global photovoltaic (PV) inverter market, capturing a commanding 45% market share. This dominant position is the result of a powerful synergy between its manufacturing supremacy and an immense internal consumption base.

- China as the Engine of Regional Growth: At the heart of the Asia-Pacific region’s dominance lies China, which has meticulously cultivated an ecosystem that supports every aspect of the solar supply chain—from raw materials and component manufacturing to module assembly and system integration. China’s 14th Five-Year Plan outlines ambitious renewable energy targets, setting a clear national directive to expand clean energy infrastructure dramatically.

- The Role of Domestic Manufacturing Giants: Meeting this colossal demand is a cohort of domestic manufacturing giants that dominate the production landscape within China and the broader Asia-Pacific region. These companies leverage advanced manufacturing capabilities, economies of scale, and integrated supply chains to supply both the domestic market and international customers. Their presence ensures a steady flow of high-quality, cost-competitive PV inverters, reinforcing the region’s market leadership.

North America Witnessing Significant Growth

North America’s photovoltaic (PV) inverter market is currently being shaped by two dominant factors, with explosive growth in utility-scale solar projects leading the way.

- Policy-Driven Push to Reshore Manufacturing: Parallel to the rapid deployment of solar capacity is a concerted policy-driven effort to rebuild and reshore North America’s solar manufacturing capabilities. The Inflation Reduction Act (IRA) has played a pivotal role in this transformation by offering substantial incentives aimed at encouraging both the deployment of clean energy and the revitalization of domestic manufacturing. This policy framework is designed to reduce reliance on foreign supply chains and bolster the resilience of the U.S. solar industry.

- Rapid Growth Driven by Utility-Scale Solar Projects: North America’s photovoltaic (PV) inverter market is currently shaped by two dominant trends: the rapid expansion of utility-scale solar projects and a strategic, policy-driven push to strengthen domestic manufacturing capabilities. The United States stands at the center of this dynamic, having achieved a record-breaking 50 gigawatts (GW) of new solar capacity installations in 2024. A significant portion of this growth—approximately 27 GWdc—originated from the utility-scale segment, underscoring the importance of large-scale solar farms in the region’s energy landscape.

Europe Dominance in the PV Inverter Market

The European photovoltaic (PV) inverter market is currently undergoing a phase of recalibration after experiencing a rapid surge driven by the recent energy crisis.

- Continued Solar Capacity: Despite the slowdown in inverter shipments and the rooftop sector’s challenges, the broader European solar market continued to demonstrate robust growth throughout 2024. The European Union successfully added an impressive 65.5 gigawatts (GW) of new solar capacity during the year, pushing the total installed capacity to 338 GW. Rather than signaling a market downturn, these figures reflect a maturing industry that is moving beyond rapid expansion toward steady, sustained development.

- Transition Toward Advanced Grid Solutions and Smart Inverters: The overall European PV inverter market is undergoing a significant transition influenced by evolving policy landscapes and technological demands. The gradual phasing out of net-metering schemes in several countries has altered the financial attractiveness of residential solar, impacting installation rates and inverter sales in that segment. Meanwhile, the increasing penetration of renewables into the power grid is driving a critical need for more advanced and intelligent grid management solutions.

Top Trends Escalating PV Inverter Market

Adoption of 1500V and 2000V Systems Redefines Utility-Scale Efficiency: The increasing adoption of higher voltage systems, such as 1500V and 2000V, is significantly transforming utility-scale solar power generation by enhancing overall efficiency. These advanced voltage platforms allow for longer strings of solar panels to be connected in series, reducing the number of inverters and associated balance-of-system components required in a project. This leads to lower installation costs, less energy loss during transmission, and improved system reliability.

Integration of Energy Storage Creates Demand for Smart Hybrid Inverters: The growing integration of energy storage solutions within solar installations has driven increased demand for smart hybrid inverters. These inverters combine the functionalities of traditional PV inverters with energy storage management, allowing seamless switching between solar power generation, battery charging, and grid interaction. Smart hybrid inverters enhance grid stability, optimize energy use, and support peak shaving and load shifting capabilities.

Shift from Central to String Inverters for Utility-Scale Projects: There is a noticeable shift in utility-scale solar projects from using central inverters to string inverters, driven by the latter’s advantages in flexibility, scalability, and efficiency. Unlike central inverters that consolidate power from large arrays of solar panels, string inverters manage smaller groups or “strings” of panels independently. This modular approach allows for easier maintenance, better performance monitoring, and improved system resilience to shading or panel failures.

Global Energy Transition Policies Drive Consistent, Long-Term Market Growth: Global energy transition policies aimed at reducing carbon emissions and promoting renewable energy sources are key drivers of consistent, long-term growth in the PV inverter market. Many countries have set ambitious targets for solar power capacity expansion as part of their commitments to climate change mitigation. Incentives such as subsidies, tax benefits, and renewable energy mandates encourage investments in solar infrastructure worldwide.

PV Inverter Market Segmentation

By Type

String photovoltaic (PV) inverters have gained significant traction in the PV inverter market, capturing over 48% of the market share. This rising demand is driven by a combination of factors that make string inverters an appealing choice for a wide range of applications, including residential, commercial, and even some utility-scale solar projects. One of the main reasons behind their growing popularity is their enhanced efficiency compared to traditional central inverters.

By End Use

Utility-scale applications continue to dominate the global photovoltaic (PV) inverter market, accounting for over 57% of the total market share. This dominance is largely attributable to the immense scale and economic benefits associated with large-scale solar power generation projects. Utility-scale solar farms typically cover extensive land areas and are engineered to produce substantial amounts of electricity, which is then fed directly into the power grid to meet the demands of entire communities or regions.

Recent Developments in the PV Inverter Market

- Ilzhöfer Launches Mini PV Systems for Metal Roofs: In July 2025, Germany-based Ilzhöfer introduced plug-in mini photovoltaic (PV) systems specifically designed for flat and trapezoidal sheet metal roofs. These compact solar arrays feature 450 W bifacial solar panels, which are capable of capturing sunlight on both sides to maximize energy generation. This innovation offers a practical and efficient solar solution tailored for building types that commonly use metal roofing, expanding the accessibility of solar power installations in various architectural settings.

- Sungrow Unveils Next-Generation Residential Energy Storage System: In July 2025, Sungrow, a global leader in photovoltaic inverters and energy storage solutions, launched its next-generation residential energy storage system (ESS) at the 2025 Southeast Asia Distribution Summit. The new ESS incorporates the advanced MG Series inverters, offering a range of power capacities from 5 kW to 10 kW. This development aims to provide homeowners with more flexible and efficient energy management options, supporting greater adoption of renewable energy through enhanced storage capabilities.

- Siemens Expands String Inverter Portfolio with Kaco New Energy Acquisition: In February 2025, Siemens completed the acquisition of the string inverter business from Kaco New Energy. This strategic acquisition is designed to strengthen Siemens’ offerings in decentralized energy systems and boost its presence in the expanding distributed generation market. The move particularly targets growth opportunities within the commercial and industrial sectors, enabling Siemens to better serve customers seeking advanced inverter solutions for localized energy production and management.

Top Companies in the PV Inverter Market

- Emerson Electric Co.

- Delta Electronics, Inc

- Eaton

- Fimer Group

- Hitachi Hi-Rel Power Electronics Private Limited

- Omron Corporation

- Power Electronics S.L.

- Siemens Energy

- SMA Solar Technology AG

- SunPower Corporation

- Other Prominent Players

Market Segmentation Overview

By Product

- String PV Inverter

- Central PV Inverter

- Micro PV Inverter

- Other PV Inverter

By End-use

- Commercial & Industrial

- Utilities

- Residential

By Geography

- North America

- Europe

- Asia-Pacific

- Latin America

- Middle East and Africa

combined with superior switching performance")

{kind=link}