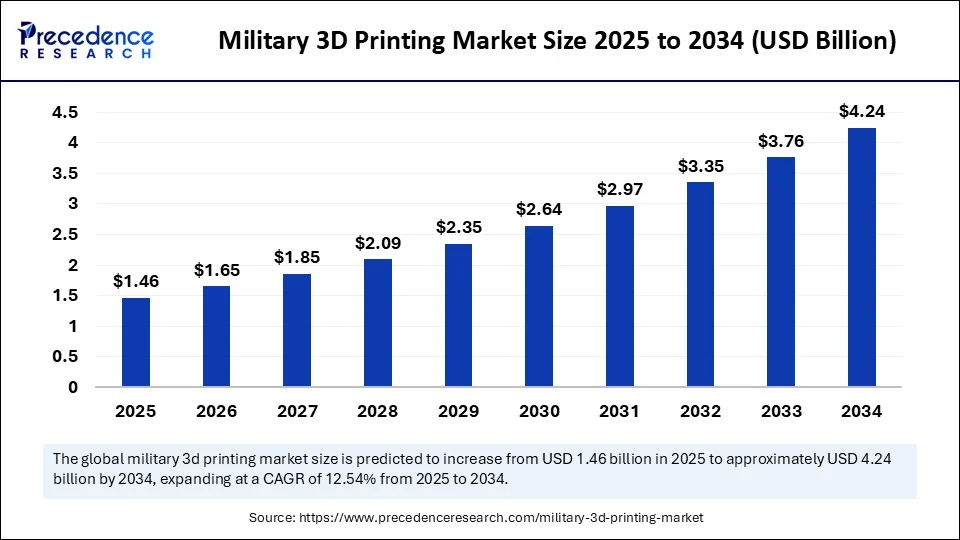

The global military 3D printing market is entering a decisive growth phase as armed forces shift from centralized procurement to on-demand, decentralized manufacturing across bases, depots, and forward operating locations. According to Precedence Research, the market was valued at USD 1.30 billion in 2024 is projected to expand from USD 1.46 billion in 2025 to USD 4.24 billion by 2034, registering a 12.54% CAGR (2025–2034). Momentum is underpinned by defense modernization programs, the need to compress lead times for mission-critical parts, and the convergence of additive technologies with AI-enabled design, process control, and predictive maintenance.

Market Overview: From Spare Parts to Strategic Readiness

The military 3D printing market spans design, prototyping, and production of spare parts, weapons components, medical equipment, and lightweight structures. By printing parts closer to the point of need, forces cut procurement cycles and reduce logistics risk, while enabling customization of mission equipment. Materials innovation, ranging from high-performance polymers to aerospace-grade metals, is broadening the addressable scope across air, land, naval, and medical theaters.

At the Intersection of 3D Printing and AI

AI is reshaping how militaries design and manufacture: algorithms simulate battlefield conditions, optimize geometries for durability and weight, and enable predictive spare-parts planning. Machine-learning based, in-process quality control reduces scrap and elevates repeatability, while autonomous manufacturing cells promise resilient production in remote or contested environments.

What’s Driving Demand Now?

Redefining Logistics Through On-Demand Manufacturing

Traditional defense procurement is expensive and slow. Additive manufacturing addresses these pain points by enabling on-site production of spares and mission-specific tools, shrinking turnaround times and limiting exposure to vulnerable supply chains. Exercises such as Project Convergence Capstone have demonstrated how autonomous resupply and forward production can cut risk and downtime while improving tempo.

Modernization and Materials

Procurement agencies are embedding additive workflows in fleet sustainment and recapitalization programs, aided by metals & alloys for high-stress components and advanced composites for lightweighting and heat resistance. As qualification frameworks mature, adoption is scaling from prototyping to flight- and field-ready parts.

Where Are the Headwinds?

Security, Standards, and Skills

Digital blueprints and machine data introduce cybersecurity risk, raising the bar for IP protection and zero-trust architectures in production. Standardization and certification of printed parts for combat environments remain challenging, particularly in metals and composites. Upfront capex and workforce training needs can slow rollout, while export controls and materials dependencies complicate supply resilience.

Opportunity Focus: Fueling Defense Modernization with Additive Innovation

- Legacy system life-extension: Print discontinued or scarce spares to reduce cannibalization and increase readiness.

- Lightweighting & performance: Use topology optimization and lattice structures for weight reduction without compromising strength, critical in aerospace and mobility.

- Forward medical care: Medical & bioprinting enables custom prosthetics, implants, and surgical guides for faster recovery in austere environments.

- Sustainability: Less waste and the potential to recycle feedstock aligns with cost and environmental targets.

- Mobile AM units: Containerized or vehicle-mounted cells bring industrial production to the tactical edge.

Regional Lens

Why North America Leads

North America’s lead stems from DoD-led adoption across aircraft sustainment and naval operations, coupled with academia–industry partnerships and a dense ecosystem of printer, software, and materials suppliers. Policy focus on readiness and self-reliance, plus frameworks for qualification and certification, are accelerating field deployment.

United States:

Can Asia-Pacific Maintain Its Fastest-Growing Trajectory?

Asia-Pacific’s ascent is fueled by rising defense budgets, technology transfer and localization, and modernization across air, sea, and land. Collaboration between local and global primes is building indigenous manufacturing capacity, while geopolitical tensions underscore the need for rapid, cost-effective sustainment.

China:

- Scaling additive across airframe, propulsion-adjacent, and armored systems with a strong push on metals and high-temperature materials.

- Focus on localizing supply (powders, filaments, composites) and expanding in-house capability for secure production.

- Broader shift from prototyping to functional spares and weight-optimized structures to extend range and payload.

India:

- Growing adoption aligns with technology absorption initiatives and a wider defense modernization agenda.

- Priority use cases include on-base spares, field tools, and UAV components, with expanding interest in medical/bioprinting for field care.

- Increasing collaboration among defense R&D units, local integrators, and AM service providers to accelerate qualification and reduce import dependencies.

Tech Deep-Dive: Why FDM Leads, And DMLS/SLM Is Rising Fast

- Fused Deposition Modeling (FDM) tops 2024 revenues thanks to cost-effectiveness, ease of use, and material flexibility across thermoplastics. Militaries favor FDM for rapid prototyping and on-site functional parts, with straightforward training and maintenance.

- DMLS/SLM (direct metal laser sintering/selective laser melting) is the fastest-growing technology as air and land platforms demand flight-worthy, high-strength metal parts with complex geometries and reduced weight, capabilities that directly impact range, payload, and survivability.

Materials: Metals Today, Ceramics & Composites Tomorrow

- Metals & Alloys (e.g., titanium, aluminum, steel) remain the workhorse for structural and high-temperature components, indispensable for aerospace and armored systems.

- Ceramics & Composites are set to grow fastest, supporting thermal shielding, protective armor, and high-performance applications where heat resistance and weight savings are paramount.

Applications: Functional Parts Dominate; Bioprinting Accelerates

- Functional parts manufacturing leads the market, enabling mission-critical replacements, from weapon grips to vehicle spares, near the point of use to curb downtime and extend equipment lifecycles.

- Medical & bioprinting is the fastest-growing application, powering custom implants, prosthetics, and tissue models tailored to individual warfighters, an advance with significant implications for battlefield trauma care.

End-Users and Distribution: Army Leads; Air Force Scales; Services Evolve

- Army stakes the largest share today, reflecting the breadth of vehicle, tool, and base-level sustainment needs across diverse terrains.

- Air Force emerges as the fastest-growing end-user, drawn by lightweight, high-performance requirements and quick-turn aerospace prototyping.

- Direct procurement currently dominates as forces keep sensitive production in-house, while additive manufacturing service providers gain traction as cost-effective partners offering specialized processes and materials without heavy internal capex.

Military 3D Printing Market Top Companies

- 3D Systems Corporation

- Stratasys Ltd.

- EOS GmbH

- ExOne (Desktop Metal)

- GE Additive

- SLM Solutions Group AG

- Renishaw plc

- Materialise NV

- HP Inc.

combined with superior switching performance")

{kind=link}