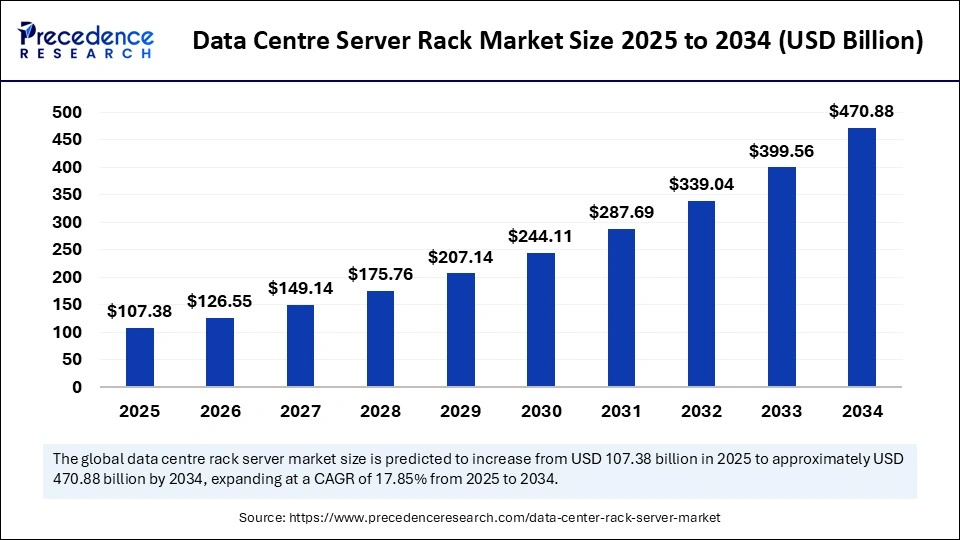

The global data center server rack market is witnessing explosive growth as digitalization accelerates worldwide. Valued at USD 107.38 billion in 2025, the market is projected to surge to USD 470.88 billion by 2034, expanding at a CAGR of 17.85%. This growth trajectory is underpinned by the rapid adoption of cloud services, the proliferation of AI-driven workloads, and the relentless expansion of hyperscale and edge data centers.

Data Center Server Rack Market Quick Insights

- Market Size (2025): USD 107.38 billion

- Forecast (2034): USD 470.88 billion

- CAGR (2025–2034): 17.85%

- Top Region (2024): North America – 38% share

- Fastest-Growing Region: Asia Pacific

- Leading Segment (Product Type): Rack enclosures – 58% share

- Emerging Trend: AI and GPU-intensive racks with advanced cooling

- Key End-Use Industry: IT & Telecom

- Fastest-Growing End-Use Industry: Healthcare

Data Center Server Rack Market Dynamics

Why is the demand for server racks surging?

The market for server racks has expanded far beyond traditional enclosures, evolving into highly integrated systems optimized for airflow, power, cooling, and density management. Hyperscale cloud providers, colocation facilities, and enterprises are investing in next-generation racks to meet rising digital workloads, AI processing demands, and sustainability goals.

- Hyperscale growth: Hyperscalers remain the largest consumers of advanced racks, driving demand for modular, high-capacity enclosures.

- Edge deployments: Edge data centers, especially for IoT and 5G applications, are growing rapidly, demanding compact yet powerful rack systems.

- Enterprise modernization: Legacy data centers are being upgraded to support virtualization, AI, and hybrid cloud workloads.

How is AI reshaping the server rack market?

AI is a game-changer for the server rack industry. High-density GPU clusters demand racks with enhanced cooling, optimized airflow, and greater power capacity. Vendors are responding with intelligent racks equipped with sensors, predictive maintenance systems, and liquid-cooling solutions. This trend is expected to accelerate as enterprises scale their AI and machine learning applications.

Regional Insights

How big U.S. Data Center Server Rack Market?

The U.S. data center server rack market size was exhibited at USD 24.24 billion in 2024 and is projected to be worth around USD 127.81 billion by 2034, growing at a CAGR of 18.09% from 2025 to 2034.

North America held the dominant position in the global data center server rack market in 2024, capturing 38% of total revenue. The United States serves as the core hub, driven by the presence of hyperscale operators such as Amazon Web Services, Microsoft Azure, Google Cloud, and Meta. These companies are investing heavily in next-generation rack enclosures optimized for AI and high-density GPU workloads. Canada is also emerging as a strong player, particularly in provinces such as Quebec and Ontario, where abundant renewable energy and favorable government incentives are fostering new data center builds. Together, the U.S. and Canada continue to set global benchmarks for large-scale, sustainable data center operations.

Asia Pacific is the fastest-growing region, poised to achieve double-digit growth throughout the forecast period. The surge is powered by rapid digital transformation, aggressive 5G rollouts, and expanding AI adoption across the region. China leads the market with state-backed infrastructure programs and a thriving cloud ecosystem driven by Alibaba Cloud, Tencent, and Huawei. India is also witnessing strong momentum, thanks to the government’s Digital India initiatives, rapid growth in digital payments, and major hyperscaler investments in cities such as Mumbai, Hyderabad, and Bengaluru. In Southeast Asia, countries like Singapore, Indonesia, and Malaysia are attracting massive data center investments due to their strategic location and booming digital economies, with Singapore being a prime hub despite its land and energy constraints.

Europe continues to prioritize energy efficiency and sustainability, making it a frontrunner in the adoption of green rack systems. The region is guided by strict regulations under the European Green Deal and carbon neutrality goals, which are accelerating demand for energy-efficient racks, liquid cooling, and modular enclosures. Germany, with its robust industrial base and Frankfurt’s role as a connectivity hub, leads the market, followed closely by the United Kingdom and Netherlands, where strong colocation and cloud service ecosystems are flourishing. Nordic countries such as Sweden and Finland are also attracting attention for their access to renewable energy and cool climates that naturally lower cooling costs.

Data Centre Server Rack Market Segments

By Product Type: Rack enclosures accounted for the largest share of the market in 2024, capturing 58% thanks to their ability to provide strong physical security, effective airflow management, and environmental protection for critical IT equipment. Meanwhile, open-frame racks are projected to register the fastest growth rate, driven by their lower cost, ease of installation, and flexibility, making them increasingly attractive for modular and scalable deployments.

By Rack Height: In 2024, ≤42U racks represented around half of the market share as they are ideal for compact deployments and small to medium-sized data centers. However, racks in the 43U–52U range are anticipated to witness the strongest growth going forward, largely due to the surging requirements of hyperscale facilities that need higher capacity and greater density to accommodate expanding workloads.

By Rack Width: Standard 19-inch racks dominated the segment with a commanding 72% share in 2024, reflecting their widespread adoption as the industry norm and compatibility with most equipment. Looking ahead, customized-width racks are expected to expand at the fastest pace, as demand grows for specialized solutions tailored to AI, machine learning, and high-performance computing (HPC) workloads that require optimized layouts and thermal management.

By Data Center Type: Hyperscale data centers remained the largest consumers of server racks in 2024, fueled by massive investments in cloud infrastructure and large-scale AI deployments. At the same time, edge data centers are forecast to grow at the fastest rate, particularly in Asia Pacific, as the rollout of 5G and IoT applications creates demand for smaller, distributed facilities closer to end-users.

By End-Use Industry: The IT & telecom sector led the market in 2024, driven by its massive data processing needs, cloud services, and the rapid expansion of connectivity solutions worldwide. However, the healthcare sector is emerging as a fast-growing end-use segment, supported by the increasing adoption of digital health technologies, AI-driven diagnostics, and electronic health records, all of which require robust and secure data infrastructure.

Market Opportunities

What opportunities lie ahead for vendors and investors?

- Green Data Centers: Sustainability initiatives are driving demand for energy-efficient racks and liquid cooling solutions.

- 5G Expansion: Edge data centers for telecom networks open lucrative opportunities for compact racks.

- Healthcare Digitization: Rapid adoption of telemedicine, imaging AI, and patient data platforms expands rack deployment in healthcare IT.

- Modular Solutions: Rising preference for plug-and-play modular racks creates opportunities for scalable deployments.

Key Players and Breakthroughs

Leading companies driving innovation include:

- Schneider Electric – advancing liquid-cooling solutions.

- Vertiv Holdings – launching AI-optimized racks for hyperscale data centers.

- Dell Technologies – focusing on modular rack enclosures for enterprise flexibility.

- Rittal GmbH – investing in energy-efficient enclosures for sustainable data centers.

Case Study: Hyperscale Upgrade

A leading U.S.-based hyperscaler recently embarked on a large-scale transition from traditional air-cooled enclosures to next-generation liquid-cooled 52U racks, designed specifically to accommodate the rising demands of AI, machine learning, and high-performance computing (HPC) workloads. The company faced growing challenges in maintaining efficiency as GPU-intensive applications pushed existing infrastructure to its limits. By integrating liquid-cooling technology directly into rack systems, the hyperscaler was able to achieve a 40% increase in compute density, allowing significantly more servers to operate within the same footprint.

Equally critical was the improvement in sustainability metrics. The adoption of liquid-cooled racks reduced overall energy consumption by 20%, cutting operational costs while aligning with the organization’s broader ESG and carbon neutrality goals. The new rack architecture also minimized cooling-related downtime, improved thermal efficiency, and extended equipment lifespan by maintaining optimal temperature thresholds.

Beyond performance gains, this upgrade demonstrated the strategic importance of innovative rack solutions in enabling digital transformation. With AI workloads expected to grow exponentially, the hyperscaler’s move positions it ahead of competitors by ensuring scalability, operational resilience, and environmental responsibility. Industry analysts view this as a bellwether for the broader market, where liquid-cooling, modularity, and intelligent monitoring systems will become standard in hyperscale environments.

This case underscores a clear shift in the global data center server rack market: operators are no longer viewing racks as static enclosures but as critical infrastructure components that directly influence compute performance, energy efficiency, and business competitiveness.

combined with superior switching performance")

{kind=link}