In the high-stakes theater of global geopolitics, the “silicon shield” usually refers to the advanced logic chips—the sub-5-nanometer brains powering Artificial Intelligence and hypersonic missiles. Yet, beneath this high-end digital canopy, a silent but equally critical revolution is reshaping the industrial landscape. It is the revolution of power—specifically, power semiconductors. These components, often overlooked in favor of their glamorous digital cousins, are the muscle of the modern world, managing the flow of electricity with a precision that dictates the efficiency of everything from a smartphone charger to a nuclear power grid.

For India, this sector represents more than just a supply chain necessity; it is a strategic imperative. As the nation accelerates toward a $1 trillion digital economy and a net-zero future by 2070, the demand for efficient energy conversion is exploding. The government’s $10 billion India Semiconductor Mission (ISM) has ignited a frenzy of activity, moving the conversation from “if” India can manufacture chips to “how fast” it can scale.

This cover story digs deep into the emerging ecosystem, exploring the tectonic shift toward Silicon Carbide (SiC) and Gallium Nitride (GaN), the localized manufacturing boom led by titans like Tata and CG Power, and the roadmap to overcoming the formidable challenges of building a fab ecosystem from scratch.

The Fabrication Frontline: Beyond the Drawing Board

Until recently, India’s semiconductor story was largely one of design prowess but manufacturing absence. That narrative flipped dramatically in 2024 and 2025. The approval of India’s first commercial fabrication plant—a massive $11 billion venture by Tata Electronics in Dholera, Gujarat, in partnership with Taiwan’s PSMC—marked the end of the wait. While Dholera focuses on logic and mixed-signal, the ripple effects for the power sector are immediate.

More specific to power electronics is the rise of the OSAT (Outsourced Semiconductor Assembly and Test) ecosystem. CG Power, in a joint venture with Japan’s Renesas Electronics and Thailand’s Stars Microelectronics, is setting up a facility in Sanand dedicated to consumer, industrial, and automotive automotive chips. Similarly, Kaynes Technology’s facility in Sanand is gearing up to package power devices. These are not mere announcements; they are the concrete pouring of a new industrial base.

The strategic logic is clear: while logic chips require the most advanced lithography, power chips require specialized packaging to handle immense heat and voltage. By securing the packaging capabilities first, India is anchoring the most labor-intensive part of the value chain, creating a pull factor for upstream wafer fabrication.

The Electrification Engine: Rewiring Mobility

The most visible driver of this manufacturing urgency is the electric vehicle (EV). The transition from internal combustion to electric drive is, at its core, a power electronics challenge. In an EV, the inverter—the device that converts the battery’s DC power to the AC power needed for the motor—is the heartbeat of the vehicle. Its efficiency dictates range; its thermal resilience dictates performance.

As the industry moves toward 800V architectures to enable ultra-fast charging, the demand for advanced power modules is skyrocketing. The efficiency gains here are not theoretical; they translate directly into kilometers added to a drive.

Ankita Padiyar, Content Manager, Polaris Market Research, captures this critical efficiency dynamic:

“Power semiconductors are vital to anything that requires fast switching and energy efficiency. One can simply look at electric vehicles; in this example, power semiconductors can show how efficiently batteries can deliver power and how quickly or slowly a vehicle can charge. The efficient working of these devices means EVs can have a longer driving range and produce less heat.”

The market statistics validate this technological dependency. As inverters become more efficient, the total cost of ownership for EVs drops, spurring adoption. The growth numbers are staggering, suggesting a market that is doubling in complexity and volume simultaneously.

According to the Listenlights research team, the trajectory is unmistakable:

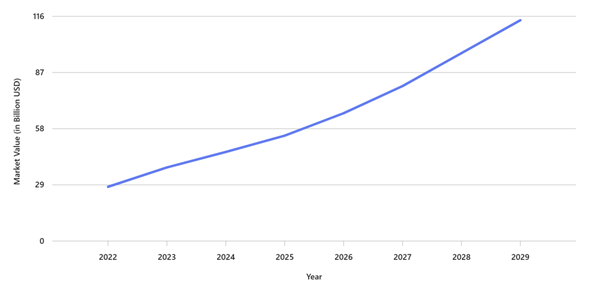

“Each EV uses 2–3 times more semiconductors than conventional vehicles, driving smarter and safer mobility. Indian EV sales grew 30% year-over-year in Q3 2025, and the sector is projected to reach $113.99 billion by 2029, highlighting rapid growth supported by advanced semiconductor technologies.”

India’s EV Sector market growth from 2022 to 2029 (Source: IBEF)

Grid Stability in the Age of Renewables

While EVs capture the headlines, the “One Sun One World One Grid” initiative places an even heavier load on India’s power electronics infrastructure. Integrating 500 GW of renewable energy by 2030 is a grid management nightmare without smart electronics. Unlike a coal plant that provides steady inertia, solar and wind are volatile.

Solar inverters, which convert the DC output of photovoltaic panels into grid-compliant AC, are the first line of defense. Modern string inverters and micro-inverters rely on high-speed switching to maximize the “harvest” of energy from the sun, even during partial shading or cloud cover. The stakes are high: in a gigawatt-scale park, a 1% efficiency loss in conversion is equivalent to powering a small town.

Ankita Padiyar highlights how quality components are non-negotiable for grid security:

“The quality of these devices has a role to play in keeping the grid stable. Power semiconductors enable quick response and allow systems to be monitored in real-time. These switches make sure that energy flows in a smooth and efficient way.”

The Physics of Efficiency: Enter SiC and GaN

To meet these grueling demands, the industry is hitting the physical limits of Silicon (Si). The atomic properties of Silicon simply cannot withstand the combination of high voltage, high temperature, and high switching frequency required by modern systems without incurring significant energy losses.

The solution lies in Wide Bandgap (WBG) materials: SiC and GaN.

- Silicon Carbide (SiC): With a bandgap three times wider than Silicon, SiC can withstand 10x higher breakdown electric fields. This makes it perfect for the high-voltage (800V+) environment of EV traction inverters and grid-tied solar inverters.

- Gallium Nitride (GaN): GaN offers exceptional electron mobility, allowing it to switch at blistering speeds. This shrinks the size of passive components (capacitors and inductors), revolutionizing power adapters and data center power supplies.

Rimma Mangusheva, Event Director, ITE Group, identifies this material shift as the definitive trend of the decade:

“The adoption of silicon carbide (SiC) and gallium nitride (GaN) is transforming power electronics by delivering higher efficiency, faster switching speeds, and greater thermal resilience. These materials outperform traditional silicon in high-voltage and high-temperature environments, making them ideal for EV drivetrains, fast chargers, renewable inverters, and compact industrial systems.”

For the design engineer, this is a paradigm shift. It is not just about swapping a chip; it is about reimagining the entire circuit topology. The ability to run hotter and faster means cooling systems can be downsized, reducing vehicle weight and increasing payload.

Yuvraj Shidhaye, Founder and Director, TreadBinary, explains the engineering implications:

“Wide bandgap materials are reshaping power devices by delivering capabilities beyond silicon. These advances are changing design practices because SiC and GaN devices switch faster, withstand higher temperatures, and limit energy loss. As adoption grows, engineers are building solutions with greater power density and reliability.”

Industry 4.0: The Automation Backbone

The ripples of this revolution extend to the factory floor. As India pushes for ‘Atmanirbhar Bharat’ in defense and manufacturing, Industry 4.0 applications are becoming standard. From robotic arms in automotive assembly lines to the Unmanned Aerial Vehicles (UAVs) monitoring borders, precision motor control is essential.

This sector is also witnessing a drive for indigenous logic to control the power. The development of the Shakti microprocessor family (based on the open-source RISC-V architecture) at IIT Madras is a prime example of India attempting to own the “brain” that controls the “muscle.”

The Listenlights research team connects this to the broader computing independence movement:

“Semiconductors power industrial automation through smart sensors, robotics, and control systems. India’s Shakti RISC-V microprocessor launch in 2025 reflects efforts toward self-reliance. AI-driven automation and edge computing are accelerating demand for high-performance chips in advanced industrial environments.”

The Challenge of Localization: The Water-Energy-Talent Trilemma

Despite the optimism, the path to a self-reliant ecosystem is paved with obstacles that are as physical as they are financial. Semiconductor fabrication is arguably the most complex manufacturing process known to humanity. It requires a “trilemma” of resources to be perfectly aligned: Ultra-Pure Water (UPW), uninterrupted high-quality power, and hyper-specialized talent.

A single fab can consume millions of gallons of water daily, which must be purified to a level where not even a single ion remains, a challenge in a water-stressed nation. Furthermore, the supply chain for raw materials, from Gallium sourcing (heavily controlled by China) to high-grade wafers, is currently non-existent in India.

Yuvraj Shidhaye details the stark infrastructural realities:

“Fabrication demands precision facilities, uninterrupted high voltage power, large volumes of ultrapure water, and advanced cleanrooms, yet only a few industrial zones offer these conditions at the required scale. Local sourcing remains limited… which increases dependence on global suppliers.”

Then there is the barrier of Intellectual Property (IP). For a home-grown design company, the cost of licensing EDA (Electronic Design Automation) tools and purchasing IP blocks for advanced nodes can bleed capital before a single prototype is made.

The Listenlights research team breaks down these economic hurdles:

“The high capital investment required to acquire or license existing intellectual property (IP) for semiconductor designs is a significant obstacle. This barrier manifests in exorbitant licensing fees and limited access to advanced nodes. Raw material bottlenecks persist, with limited access to high-purity silicon wafers… forcing import dependence.”

Rimma Mangusheva reinforces the need to address the maturity gap in the ecosystem:

“Indian manufacturers face three main challenges: infrastructure, ecosystem maturity, and supply chain dependency. The domestic fabrication ecosystem is still developing, with limited access to 300 mm fabs and advanced lithography.”

The Way Forward: A Collaborative Blueprint

How does India navigate these choppy waters? The answer lies in breaking the silos. In the analog and power world, the feedback loop between the chip designer, the fab, and the end-user (system integrator) is critical. Unlike digital chips, which are often “one size fits all,” power chips must be tuned to the specific thermal and voltage realities of their application.

Ankita Padiyar emphasizes that isolation is the enemy of progress:

“The operation of teams in silos slows down progress. Collaborative R&D clusters can support testing and material research. Partnerships between fabs and chip designers can accelerate development… This is highly important for SiC and GaN semiconductor devices, where design and manufacturing are closely linked.”

Government policy acts as the binding agent for this collaboration. The initial success of the PLI (Production Linked Incentive) schemes and the DLI (Design Linked Incentive) scheme has created a foundation, but the industry is looking for stability. Semiconductor investment cycles are measured in decades, not years.

Rimma Mangusheva prescribes a stability-focused policy approach:

“Policies must focus on long-term incentives for fabs, packaging units, and design houses, ensuring stability and confidence for private investors. Expanding public–private R&D programs in areas like SiC/GaN materials will accelerate technology leadership.”

Finally, the hardware is only as good as the human mind designing it. The talent gap, specifically in device physics and process engineering, is the bottleneck that money alone cannot solve.

Yuvraj Shidhaye highlights the talent imperative:

“Research and skills are equally important. To turn this work into production, India needs deeper university–industry collaboration, shared pilot lines, and specialised training in wafer processing, epitaxy, packaging, and module engineering.”

Conclusion

The narrative of India’s semiconductor journey has shifted from skepticism to cautious execution. The demand engines, EVs, renewables, and industrial automation, are firing in sync. The technology pathways, SiC and GaN, are clear. While the challenges of infrastructure and supply chain depth remain formidable, the “Silent Revolution” of power semiconductors is no longer just a possibility; it is an active construction project.

As the Listenlights research team concludes:

“Building India as a global power semiconductor hub requires three pillars: strong policy support, focused research, and extensive skill development. The India Semiconductor Mission offers up to 50% fiscal support… while dedicated semiconductor zones in Dholera and Noida ensure streamlined access to land, power, and water.”

India is powering up. The world is watching.

combined with superior switching performance")

{kind=link}