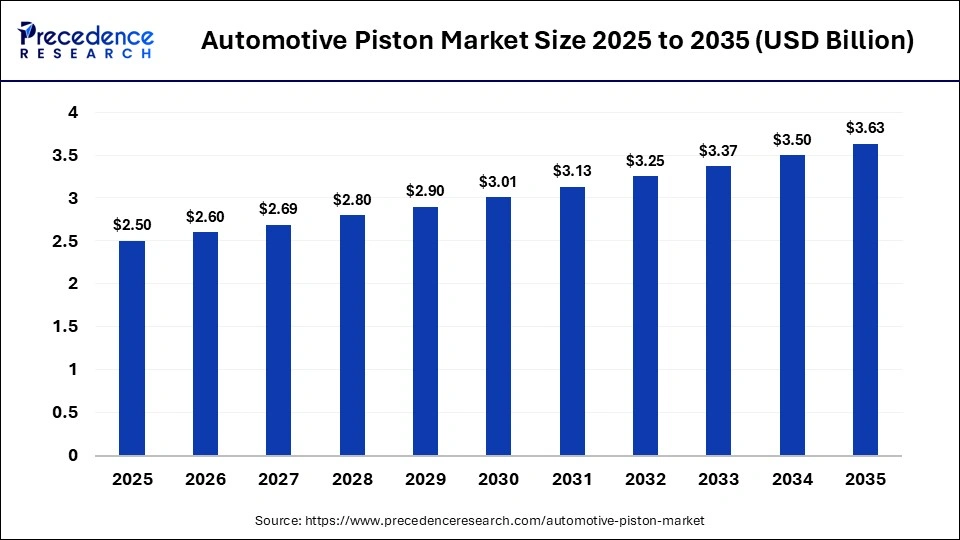

The global automotive piston market size accounted for USD 2.50 billion in 2025 and is predicted to increase from USD 2.60 billion in 2026 to approximately USD 3.63 billion by 2035, expanding at a CAGR of 3.80% from 2026 to 2035. Market growth is driven by rising global vehicle production, regulatory emission targets, lightweight material adoption, and innovation in engine design.

Key Takeaways

- Asia-Pacific dominated the global automotive piston market with a share of approximately 40% in 2025 and is expected to grow at the fastest CAGR of 4.5% in the market during the forecast period.

- By competent type, the piston segment held a dominant position in the market with a share of approximately 49% in 2025.

- By component type, the piston pins segment is expected to grow with the highest CAGR of 3.4% in the market during the studied years.

- By vehicle type, the passenger vehicles segment dominated the market with a share of approximately 60% in 2025.

- By vehicle type, the commercial vehicles segment is expected to expand rapidly with a CAGR of 3.5% in the coming years.

- By material type, the aluminum pistons segment accounted for a considerable revenue share of approximately 58% in the market in 2025 and is expected to grow with the highest CAGR of 3.6% in the market during the studied years.

- By engine/fuel type, the gasoline segment led the global market with a share of approximately 45% in 2025.

- By engine/fuel type, the hybrid/alternative fuels segment is expected to gain the highest market share with a CAGR of 3.8% between 2026 and 2035.

Automotive Piston: Engine Efficiency and Performance

The automotive piston market consists of components used in internal combustion engines to convert combustion pressure into mechanical motion. Pistons, piston rings, and piston pins are critical for engine performance, fuel efficiency, and emission control in passenger and commercial vehicles . Product development strategies are being redesigned due to the increase in demand for lightweight and high-strength materials. With the rise of EVs, we still produce hybrid and ICE cars, which allows us to maintain a high demand in the world.

What is the Role of AI in the Automotive Pistons?

The application of artificial intelligence (AI) is changing the piston design by means of sophisticated simulation and predictive modelling. AI tools are optimized to be used in improving the efficiency of the piston geometry, thermal resistance, and composition of materials. AI and machine learning (ML) algorithms can analyze vast amounts of data and predict potential defects in pistons caused by overheating, excessive wear, or mechanical failure, enabling real-time updates. AI is also used in smart manufacturing systems to detect defects and achieve accuracy in machining. Another benefit of predictive analytics is the maintenance, forecasting, and product lifecycle management.

Regional Outlook of the Automotive Pistons Market

Asia Pacific

Asia-Pacific held a major market share of approximately 40% and is expected to be the fastest-growing with a CAGR of 4.5% in the market. This can be attributed to the fact that it has a big automotive manufacturing base. The markets are growing due to rapid urbanization, increasing disposable incomes, and high vehicle demand. The region enjoys economic production factors and large supply chains. More adoption of hybrid cars will boost the demand for pistons even more. The government policies that favor local motor-industry production drive the growth. Increasing exports of vehicles and components maintain long term market dominance.

North America

North America is expected to grow at a considerable CAGR in the upcoming period, due to technological advancements and the growth of hybrid cars. The increasing demand for SUVs and light trucks is favorable for the consumption of pistons. The existence of high emphasis on fuel efficiency and emission cut promote the development of high-tech piston materials. The availability of larger automotive OEMs enhances local production. The market for engine overhauls is also an after-market, which is one reason why the market grows steadily. Investments in automation and research and development contribute to competitiveness.

Automotive Pistons Market Companies

MAHLE GmbH

MAHLE GmbH is a global leader in the automotive piston market, offering advanced piston technologies for passenger and commercial vehicles with a strong focus on lightweight and high-performance designs. The company dominates the market through innovation in thermal management and fuel-efficient engine components.

Tenneco Inc.

Tenneco Inc., through its Federal-Mogul division, is a key manufacturer of pistons and piston rings, serving OEMs and aftermarket segments worldwide. The company emphasizes durability, emission reduction, and advanced coating technologies in piston systems.

Aisin Seiki Co., Ltd.

Aisin Seiki Co., Ltd. (Aisin Corporation) is a major player in the automotive piston market with a strong global presence and diversified automotive component portfolio. It focuses on high-volume production, precision engineering, and integration with advanced powertrain systems.

Hitachi Astemo, Ltd.

Hitachi Astemo, part of the Hitachi group, provides advanced engine and mobility solutions, including piston-related components designed for efficiency and sustainability. The company integrates electrification and traditional engine technologies to support evolving automotive demands.

Toyota Industries Corporation

Toyota Industries Corporation plays a supporting role in the automotive piston ecosystem through its engine and component manufacturing capabilities. It leverages strong integration within the Toyota Group to deliver high-quality, reliable engine components for global automotive applications.

Rheinmetall AG (KSPG / Kolbenschmidt)

Rheinmetall AG, through its Kolbenschmidt (KS) division, is a leading manufacturer of pistons, engine blocks, and related components with strong expertise in emission reduction technologies. The company is known for innovation in lightweight pistons and advanced combustion solutions.

Segmental Insights of the Automotive Pistons Market

Component Type Insights

The piston segment dominated the market with a share of approximately 49% in 2025, since it is the most moving part in internal combustion engines. Any engine that is based on combustion demands several pistons, which have an immediate high-volume requirement. The efficiency and durability of pistons are continuously improved through new technologies of lightweight alloys and coatings. The rising manufacturing of passenger vehicles across the world adds more strength to the segment leadership. This is also because replacement demand in engine overhauls also propels the segment’s growth.

Vehicle Type Insights

The passenger vehicles segment held the largest market share of approximately 60% in 2025 because it is highly produced across the globe. Increasing urbanization and mobility among individuals require further sales of vehicles. The high emission standards promote the use of modern technologies. Demand is also supported by regular servicing of engines and replacement. The production of hybrid passenger cars also helps in the long-term increase.

Material Type Insights

The aluminum pistons segment contributed the biggest market share of approximately 58% and is expected to expand rapidly in the market with a CAGR of 3.6% in the coming years, which has lightweight qualities and good thermal conductivity. They enhance fuel efficiency by decreasing the weight of the engines and improving heat dissipation. They can be used in hybrid and commercial applications because of increased longevity. Cost-effectiveness and ease of production also contribute to the usage by the majority. They are gaining momentum because of the growing pressure to have down-sized but powerful engines. Alloys of aluminum are also sufficient in terms of strength to work in most passenger cars. Segment leadership is ensured by continuous investments in alloy composition.

Engine/Fuel Type Insights

The gasoline segment accounted for the highest market share of approximately 45% in 2025, due to high production volumes of cars powered by gasoline. The technological growth is working towards the enhancement of the efficiency of combustion and minimizing emissions. Developing economies are still heavily dependent on gasoline cars. In the mature markets, replacement demand further supports the segment.

combined with superior switching performance")

{kind=link}