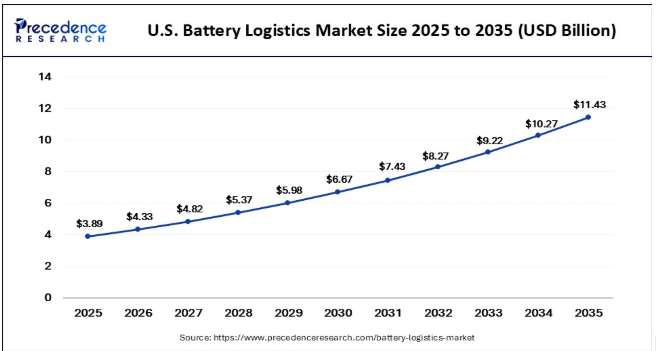

The U.S. battery logistics market size was valued at USD 3.89 billion in 2025 and is projected to grow from USD 4.33 billion in 2026 to approximately USD 11.43 billion by 2035, registering a CAGR of 11.38% during the forecast period from 2026 to 2035. The market growth is primarily driven by the rapid expansion of electric vehicle production, increasing domestic battery manufacturing, and the rising demand for specialized transportation and storage solutions for lithium-ion batteries.

Key Takeaways

- By batter type, the lithium-ion batteries segment held the largest share of the market in 2025.

- By logistics service, the transportation services segment dominated the market in 2025.

- By transportation mode, the multimodal transport segment is expected to grow at a significant CAGR during the forecast period.

- By application, the energy storage systems segment is expected to grow with a notable CAGR during the forecast period.

- By battery lifecycle, the finished battery distribution segment led the market in 2025.

- By end user, the energy & utility companies segment is expected to grow at the fastest rate over the forecast period.

Market Overview

The U.S. battery logistics market encompasses transportation, warehousing, packaging, inventory management, reverse logistics, and recycling services that support the safe and efficient movement of batteries across the supply chain. It serves battery manufacturers, EV companies, energy storage providers, and electronics manufacturers while ensuring regulatory compliance, safety, and traceability.

The market is witnessing strong growth due to the rapid expansion of the electric vehicle (EV) industry, increasing domestic battery manufacturing, rising deployment of energy storage systems, and investments in battery gigafactories. Growing demand for specialized logistics solutions, along with battery recycling and end-of-life management services, continues to create significant growth opportunities.

How is AI Influencing the U.S. Battery Logistics Market?

Artificial intelligence (AI) is transforming the U.S. battery logistics market by optimizing route planning, improving inventory management, and enhancing supply chain visibility. AI-powered analytics enable real-time battery monitoring, demand forecasting, and warehouse optimization, helping reduce transportation costs and delivery delays. In addition, AI-driven predictive maintenance improves the safe handling of lithium-ion batteries while ensuring compliance with hazardous material regulations. The integration of AI with IoT and advanced tracking technologies is further strengthening operational efficiency, supply chain resilience, and end-to-end traceability across the battery logistics ecosystem.

State-Level Analysis of the U.S. Battery Logistics Market

California

California held a significant position in the U.S. battery logistics market because of its robust ecosystem for electric vehicles, extensive battery manufacturing operations, and aggressive clean energy legislation. The state’s battery transportation and distribution operations are further supported by the existence of large ports, battery producers, and top EV manufacturers. Furthermore, battery demand and related logistical activities are still being driven by California’s aggressive zero-emission vehicle ambitions.

Massachusetts

Massachusetts is emerging as a prominent market because of increased funding for energy storage initiatives, battery research, and renewable energy technology. Demand for battery logistics services is anticipated to rise due to the state’s robust innovation ecosystem and growing emphasis on decarbonization. Research partnerships and supportive state regulations are bolstering industry expansion even more.

Texas

Texas represents a key market due to substantial investments in EV-related infrastructure, expanding battery production facilities, and increasing capacity for renewable energy. The state’s position in the battery logistics sector is further strengthened by its advantageous location, extensive transportation system, and welcoming business climate. The market is expanding because of rising investments in large-scale energy storage projects.

North Carolina

North Carolina is witnessing substantial growth in the market because of growing expenditures in EV supply chain facilities and battery production facilities. During the projection period, market expansion is anticipated to be accelerated by the state’s favorable policies, trained workforce, and growing industrial investments. Additionally, it is anticipated that the state’s demand for logistics would increase due to the existence of new battery manufacturing projects.

U.S. Battery Logistics Market Companies

- DHL Supply Chain: DHL Supply Chain provides specialized battery logistics services, including hazardous material transportation, warehousing, and reverse logistics for lithium-ion batteries, supporting EV and energy storage supply chains across the U.S. DHL Group reported approximately EUR 84.2 billion (around USD 91 billion) in revenue in 2025.

- FedEx Corporation: FedEx offers comprehensive battery logistics solutions through its express, freight, and supply chain networks, ensuring compliant transportation and distribution of lithium-ion batteries. FedEx Corporation generated approximately USD 88.9 billion in revenue for fiscal 2025.

- UPS Supply Chain Solutions: UPS Supply Chain Solutions delivers end-to-end battery logistics services, including secure transportation, inventory management, customs brokerage, and reverse logistics for EV battery manufacturers. UPS Inc. recorded approximately USD 91.1 billion in revenue in 2025.

- Kuehne+Nagel: Kuehne+Nagel specializes in compliant battery transportation, contract logistics, and warehousing services, supporting the expanding U.S. electric vehicle and battery manufacturing ecosystem. Kuehne+Nagel Group reported approximately CHF 24.8 billion (around USD 30 billion) in revenue in 2025.

- DB Schenker: DB Schenker provides multimodal transportation, specialized packaging, and hazardous goods logistics for lithium-ion batteries, helping strengthen battery supply chains in North America. DB Schenker generated approximately EUR 20.5 billion (around USD 22 billion) in revenue in 2025.

- DSV A/S: DSV A/S offers integrated battery logistics solutions, including air, sea, road freight, warehousing, and regulatory-compliant handling for battery manufacturers and EV companies. DSV A/S reported approximately DKK 167 billion (around USD 24 billion) in revenue in 2025.

Segmental Insights of the U.S. Battery Logistics Market

Battery Type Insights

The lithium-ion batteries segment dominated the U.S. battery logistics market with the largest share in 2025, as lithium-ion batteries are widely used in energy storage systems, consumer devices, and electric cars. The demand for specialist logistics services for lithium-ion batteries was further reinforced by the swift growth of domestic battery manufacturing facilities and rising investments in EV production. Additionally, the segment’s dominance was reinforced by favorable government regulations that encouraged local battery production.

Logistics Service Insights

The transportation services segment dominated the U.S. battery logistics market while holding a major share in 2025. This is because battery components, raw materials, and completed batteries are transported in large quantities along the supply chain. Segment dominance was further reinforced by battery makers’ requirement for just-in-time delivery and specialized transportation of hazardous materials. Additionally, the demand for transportation services was raised by the growth of both domestic and international battery trade.

Transportation Mode Insights

The road transportation segment led the U.S. battery logistics market with the largest share in 2025. This is because of its extensive transportation network, operational flexibility, and ability to support door-to-door delivery across battery manufacturing, assembly, distribution, and recycling facilities. The rapid expansion of electric vehicle (EV) production and battery gigafactories across the U.S. has significantly increased the movement of lithium-ion batteries and battery components through trucking networks, making road transport the preferred logistics mode.

Application Insights

The electric vehicles (EVs) segment dominated the market with the largest share in 2025. This is because EV production and sales have significantly increased in the U.S. The demand for logistics was further boosted by growing investments in local EV battery production and government incentives encouraging car electrification. The segment’s position was further reinforced by the construction of additional EV assembly facilities.

Battery Lifecycle Insights

The finished battery distribution segment dominated the U.S. battery logistics services market with the largest share in 2025. This is because manufacturing facilities are shipping more completed battery packs to wholesalers, energy storage companies, and automakers. The expansion of the segment was further aided by the increasing number of battery manufacturing facilities in the United States. The segment’s growth was further reinforced by growing demand for safe and prompt battery delivery.

End User Insights

The automotive OEMs segment led the U.S. battery logistics market with the largest share in 2025. This is because the manufacturing of electric vehicles has increased significantly. As a result, automakers are purchasing more battery packs. Increased logistics activity was also a result of strategic alliances between automakers and battery producers. Additionally, the need for storage and transportation has grown due to the localization of battery supply chains.

combined with superior switching performance")

{kind=link}