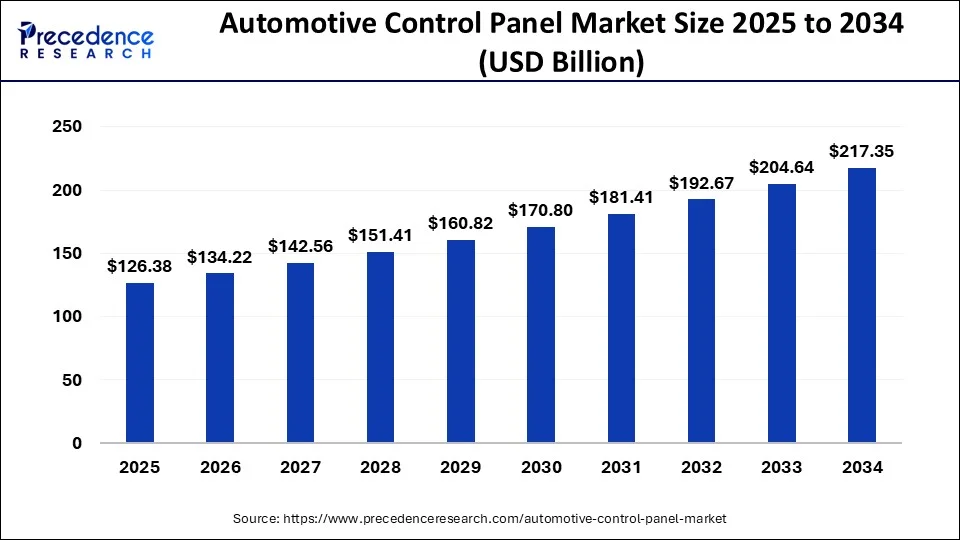

According to Precedence Research, the global automotive control panel market size is expected to attain around USD 217.35 billion by 2034 from USD 118.99 billion in 2024, with a CAGR of 6.21%.

From capacitive touchscreens to rotary knobs seamlessly integrated with ADAS and infotainment systems, the automotive control panel has evolved from a functional cluster to a digital command hub central to the driving experience. With OEMs and Tier-1 suppliers investing in personalization and human-machine interface (HMI) innovations, the market is primed for robust expansion across both passenger and commercial vehicle segments.

Key Highlights of the Automotive Control Panel Market:

- Asia Pacific dominated the market in 2024, accounting for the largest share of 37%, while North America is expected to experience steady growth during the forecast period.

- Based on type, the manual control panel segment led the market in 2024 with a 39% share, whereas the touchscreen control panel segment is poised for notable growth in the coming years.

- In terms of application, passenger cars held the largest market share at 54% in 2024, while the light commercial vehicle (LCV) segment is expected to expand at a considerable rate throughout the forecast period.

What’s Driving the Market Forward?

Is the demand for smarter vehicles reshaping the future of control panels?

Absolutely. Automakers are in a race to redefine user interaction. As dashboard control panels become increasingly centralized and software-defined, traditional mechanical buttons are being replaced with customizable touchscreen interfaces. With growing consumer expectations for seamless digital experiences, control panels now act as command centres integrating navigation, entertainment, climate control, safety, and connectivity.

Moreover, the shift toward electric and autonomous vehicles is prompting car manufacturers to adopt sleeker, software-integrated panels that support voice assistance, AI, and gesture control. This trend is particularly strong in Asia Pacific, which led the market with a 37% share in 2024, thanks to booming car production in China, India, Japan, and South Korea.

Regional Outlook: Where is the Market Headed?

Asia Pacific emerged as the dominant region in 2024, accounting for more than 37% of global revenue driven by large-scale automotive production hubs, rising income levels, and rapid urbanization.

North America is projected to witness the fastest CAGR over the forecast period, fueled by advanced infotainment integration and the expansion of the EV ecosystem in the U.S. and Canada. Meanwhile, Europe remains a stronghold for premium vehicles with complex digital control interfaces.

What Are the Key Trends and Opportunities?

Can HMI and AI integration unlock new growth horizons for control panels?

Indeed, the integration of artificial intelligence and machine learning into automotive control systems is redefining user experience. Smart panels that adapt based on driver behavior, ambient conditions, and location are already under development. Companies are also exploring haptic feedback technologies, gesture recognition, and multi-modal interaction interfaces, which are expected to become standard in future car models.

Another emerging trend is the modular control panel architecture, enabling easier software updates and cost-efficient design customizations across multiple vehicle platforms.

Innovations from Market Leaders

Top players like Hyundai Mobis, Faurecia, and Continental AG are heavily investing in advanced infotainment modules and 3D curved display panels. For instance:

- Continental AG recently showcased its ShyTech Display, an ultra-slim, invisible control panel that activates upon touch.

- Hyundai Mobis developed an Integrated Center Stack (ICS) that merges HVAC and multimedia control into a singular glass interface.

- Faurecia is pushing modular cockpit electronics aligned with Level-3 autonomous driving.

Challenges and Cost Pressures

Are OEMs struggling with cost-performance trade-offs?

Yes. One of the primary challenges is balancing cost efficiency with innovation—especially as Tier-1 suppliers face pressure to deliver high-performance HMI components within strict cost parameters. Additionally, chip shortages, supply chain disruptions, and the need for cross-platform software compatibility have made mass production of sophisticated control panels complex.

Case Study: EV Dashboard Transformation

In 2023, a leading EV startup in India partnered with a Tier-1 supplier to revamp its entire dashboard interface. By adopting a capacitive touch control panel with OTA capabilities, they were able to reduce the BOM (bill of materials) by 18%, improve customer satisfaction scores by 25%, and enable real-time feature upgrades—demonstrating the ROI of investing in next-gen control panels.

Segmental Insights

- Vehicle Type: Passenger cars lead the market due to rising demand for tech-rich dashboards, while commercial vehicles adopt control panels for enhanced safety and driver assistance.

- Component: Rotary switches and touchpads dominate for their usability, with control knobs still favored in mid-range vehicles.

- Control Panel Type: Manual panels remain common in cost-sensitive markets, whereas push button and touch-sensitive panels are gaining popularity in premium vehicles.

combined with superior switching performance")