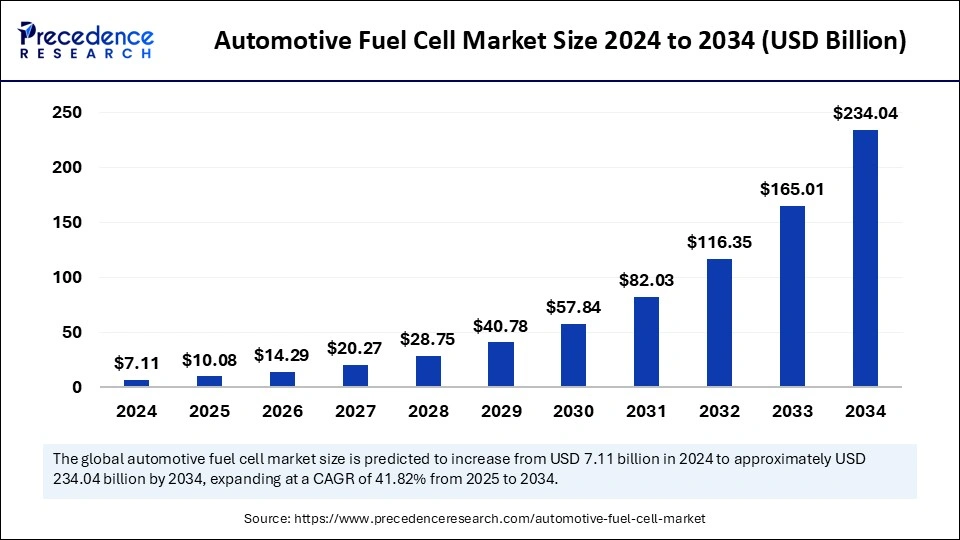

The global automotive fuel cell market is undergoing a massive transformation, poised to shift from a niche technology to a mainstream clean mobility solution. In 2024, the market was valued at USD 7.11 billion, and it is projected to grow significantly in the coming years. According to Precedence Research, the market is forecast to increase from USD 10.08 billion in 2025 to approximately USD 234.04 billion by 2034, expanding at a remarkable compound annual growth rate (CAGR) of 41.82% during the forecast period.

This exceptional growth is driven by global climate initiatives, technological advancements in hydrogen-powered vehicles, and a growing consensus among automakers and governments to invest in zero-emission mobility. Regions like Asia-Pacific continue to lead the adoption wave, supported by large-scale hydrogen infrastructure projects in Japan, China, and South Korea. Meanwhile, North America and Europe are rapidly catching up, fueled by green hydrogen investments and regulatory pressure on commercial vehicle emissions.

What Are Automotive Fuel Cells and Why Are They Important?

Automotive fuel cells are advanced electrochemical devices that convert hydrogen gas into electricity, emitting only water and heat as byproducts. Unlike battery electric vehicles (BEVs) that rely on stored electricity, fuel cell vehicles (FCVs) generate power on demand, offering a continuous supply of electricity as long as hydrogen fuel is available. This refueling capability gives FCVs a unique advantage in terms of range and turnaround time.

The role of automotive fuel cells is becoming increasingly vital in the pursuit of zero-emission transportation, especially for long-haul trucks, commercial fleets, and heavy-duty applications where batteries alone are insufficient. Offering quiet operation, high efficiency, and no tailpipe emissions, fuel cells represent a cornerstone technology for the global energy transition.

Why Asia Pacific Dominates the Automotive Fuel Cell Market

The Asia Pacific automotive fuel cell market size was USD 5.26 billion in 2024 and is predicted to reach around USD 174.36 billion by 2034, at a CAGR of 41.82% from 2025 to 2034.

Government Policy and Subsidies

Asia Pacific countries, particularly China, Japan, and South Korea—are actively promoting fuel cell electric vehicles (FCEVs) through subsidies, infrastructure development, and national hydrogen strategies.

- China introduced a Hydrogen Industry Development Plan (2021–2035) aiming to establish:

- 50,000 hydrogen FCEVs by 2025.

- 1000+ hydrogen refueling stations by 2030.

- Japan set a target of:

- 800,000 FCEVs on the road by 2030.

- Supported by the Strategic Road Map for Hydrogen and Fuel Cells.

- South Korea committed to:

- Producing 6.2 million FCEVs by 2040.

- Building 1,200 hydrogen fueling stations by 2040 under its Hydrogen Economy Roadmap.

These policies include financial incentives, R&D funding, and public-private partnerships, making the region a hotbed for fuel cell innovation and adoption.

2. Automotive Giants & Technological Innovation

Asia Pacific is home to global automotive leaders who are pioneering hydrogen fuel cell technologies.

- Toyota (Japan) – Manufacturer of the Mirai, one of the most commercially successful FCEVs globally.

- Hyundai (South Korea) – Leading the market with NEXO, and developing hydrogen-powered commercial trucks and buses.

- SAIC Motor (China) – Rapidly scaling domestic fuel cell production with government support.

These companies not only manufacture FCEVs but also invest heavily in infrastructure, R&D, and global partnerships.

Robust Hydrogen Infrastructure Development

Fuel cell adoption is directly linked to the availability of hydrogen fueling infrastructure. Asia Pacific leads in:

- Hydrogen refueling stations:

- Japan: Over 160 operational stations in 2024.

- South Korea: 180+ stations, expanding rapidly.

- China: Plans to build 1,200+ stations by 2030.

Economic and Industrial Ecosystem

Asia Pacific’s advanced manufacturing ecosystem enables large-scale production of:

- Fuel cell stacks

- Hydrogen storage systems

- Power electronics

This lowers the cost of FCEV production and accelerates commercialization compared to other regions.

Strategic Collaborations and Export Potential

The region is actively forming international collaborations to strengthen its hydrogen economy:

- South Korea partners with Saudi Arabia for hydrogen fuel imports.

- China and Japan are engaged in joint hydrogen research and technology sharing.

These partnerships ensure a steady hydrogen supply and enable regional export leadership.

Key Drivers of Asia Pacific Dominance in Fuel Cell Vehicles

| Factor | Details & Statistics |

| Government Support | China: 50,000 FCEVs by 2025, 1,000+ H₂ stations; Japan: 800,000 FCEVs by 2030 |

| Leading Automakers | Toyota (Mirai), Hyundai (NEXO), SAIC – fuel cell tech leadership |

| Hydrogen Infrastructure | Japan: 160+ H₂ stations; Korea: 180+; China: plans for 1,200+ by 2030 |

| Production Ecosystem | Low-cost manufacturing of fuel cell components, R&D centers in APAC |

| Strategic Partnerships | Korea–Saudi Arabia hydrogen trade; China–Japan technology collaboration |

| Technology & R&D Investment | Multi-billion dollar investments by Toyota, Hyundai, and government R&D grants |

Fuel Cell Vehicle (FCV) Technology Landscape

The most prevalent type of fuel cell used in vehicles is the Proton Exchange Membrane Fuel Cell (PEMFC). Known for their low operating temperatures and high power density, PEMFCs are ideal for automotive use. Recent advancements in this space have focused on enhancing fuel cell durability, optimizing thermal management, and improving power output per volume. These enhancements make fuel cells more reliable and efficient for everyday transportation needs.

Many manufacturers are also adopting hybrid architectures that combine fuel cells with battery packs. This hybridization allows for energy recovery during braking, peak power assistance during acceleration, and smoother performance across driving cycles. Hybrid FCVs are particularly effective in urban environments where stop-and-go traffic is frequent and regenerative braking can significantly boost overall energy efficiency.

Hydrogen storage is another critical component of FCV design. Vehicles typically store hydrogen in high-pressure tanks (350 to 700 bar) to maximize range while maintaining safety. Emerging storage technologies, such as cryo-compressed hydrogen and liquid organic hydrogen carriers, are being explored to increase volumetric energy density and simplify fuel logistics. These technological advancements are laying the groundwork for mass adoption of fuel cell vehicles across different transportation segments.

What Are the Different Types of Fuel Cells in Automotive Applications?

The automotive fuel cell market is categorized by type into PEMFC (Proton Exchange Membrane Fuel Cells), PAFC (Phosphoric Acid Fuel Cells), and Others. Among these, PEMFCs dominate the landscape due to their lower operating temperature, quick start-up times, compact design, and high power density, attributes that are especially critical for automotive applications. These cells are ideal for both passenger and commercial vehicles. PAFCs, while more stable and suitable for larger-scale or stationary applications, are gaining ground in heavy-duty vehicle categories. The “Others” category encompasses emerging or niche fuel cell types, including SOFCs and MCFCs, which may play more substantial roles in the future as efficiency and cost parameters improve.

How Does Power Rating Influence Market Trends?

Fuel cell vehicles are segmented by power output ratings into Below 100 kW, 100–200 kW, and Above 200 kW. Vehicles with below 100 kW fuel cells are generally passenger cars and compact models, where moderate power and high efficiency are vital. The 100–200 kW segment is witnessing rapid growth, as it aligns well with mid-sized sedans and SUVs that require a balance of performance and range. Above 200 kW systems are tailored for heavy-duty applications like buses and long-haul trucks, where higher torque and extended operation are essential. Growth in the 100+ kW segments reflects increasing adoption of hydrogen-powered buses and trucks for public and commercial transportation.

What Vehicle Types Are Driving Fuel Cell Adoption?

Based on vehicle category, the automotive fuel cell market is segmented into Passenger Vehicles, Light Commercial Vehicles (LCVs), Buses, and Trucks. Passenger vehicles currently account for a significant share, bolstered by growing investments from automakers like Toyota, Honda, and Hyundai. These cars are becoming more mainstream in markets like South Korea, Japan, and California due to supportive policies and fueling infrastructure. Light Commercial Vehicles are gaining traction as fleet operators seek eco-friendly solutions for urban logistics and last-mile delivery. On the other hand, fuel cell buses are being increasingly adopted by city transit systems aiming to reduce emissions while maintaining range and power needs. The truck segment is poised for high growth in the long term, especially as major manufacturers pilot hydrogen-based long-haul freight solutions to address the limitations of battery electric alternatives in heavy-load scenarios.

Automotive Fuel Cell Market Key Players

- Ballard Power Systems

- Plug Power

- Hydrogenics

- Hyundai Motor Company

- Nuvera Fuel Cells, LLC

- PowerCell Sweden AB

- Horizon Fuel Cell Technologies

- Nedstack Fuel Cell Technology

- AVL

- ElringKlinger

- Intelligent Energy

- Pragma Industries

- Umicore

- Valmet Automotive

- Air Liquide

Hydrogen Infrastructure: The Backbone of the FCV Ecosystem

Current Global Refueling Network

Hydrogen fueling infrastructure remains uneven but is expanding rapidly:

- Japan: Over 160 stations (backed by the H2 Mobility initiative)

- South Korea: Over 100 stations with plans for 300+ by 2030

- Germany: Nearly 100 operational stations under H2 Mobility Germany

- U.S. (California): 55+ retail stations operational, with more in planning

However, refueling availability remains a critical bottleneck, particularly outside urban centers.

Investment Trends in Green Hydrogen

Major companies and governments are investing in green hydrogen production, using solar, wind, and hydropower. Key examples:

- Air Liquide, Linde, and Plug Power are scaling electrolyzer plants.

- Saudi Arabia’s NEOM plans a $5 billion green hydrogen plant.

- The Hydrogen Council forecasts investments of $500 billion by 2030 across the hydrogen value chain.

Public-Private Collaborations

To bridge infrastructure gaps, collaborations are emerging between:

- Automakers and fuel providers

- Governments and clean tech startups

- Research institutes and transportation authorities

Case Study: Japan’s H2 Mobility Initiative

Japan leads the world in coordinated hydrogen development. The Japan H2 Mobility consortium (JHyM) includes:

- Automakers: Toyota, Honda, Nissan

- Fuel companies: ENEOS, Iwatani

- Government bodies and banks

Together, they’ve built an ecosystem with subsidized refueling, vehicle rollouts, and customer awareness programs

combined with superior switching performance")

{kind=link}