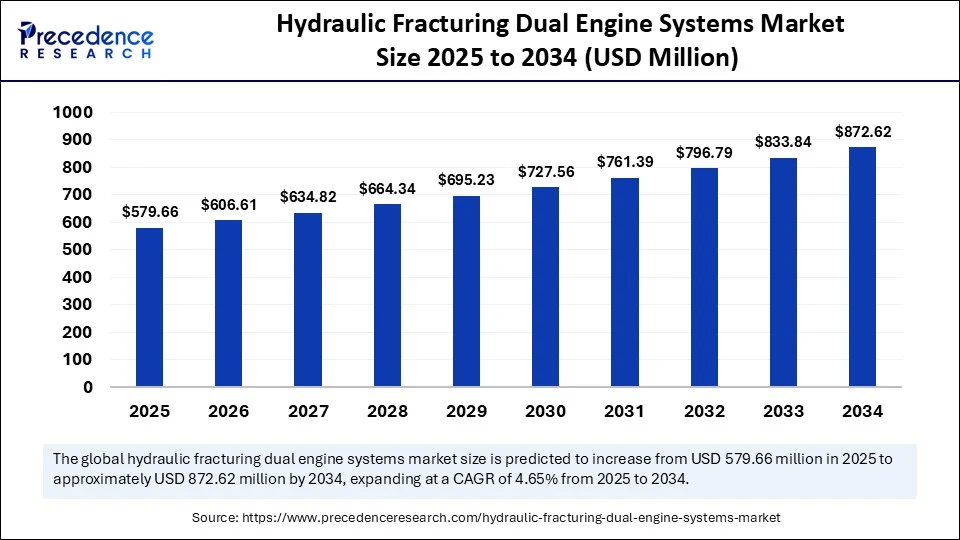

Fracturing Dual Fuel Engine Systems market size reached USD 553.9 million in 2024 and is projected to be worth around USD 872.62 billion by 2034, registering a CAGR of 4.65% from 2025 to 2034. As the global energy landscape pivots toward cleaner, cost-efficient solutions, Hydraulic Fracturing Dual Fuel Engine Systems are becoming central to the oilfield’s evolution. A new report by Precedence Research projects that this high-efficiency, Hydraulic.

These systems, which operate on a mix of natural gas and diesel, offer a smarter and more sustainable alternative for hydraulic fracturing (fracking) operations, especially in shale-rich territories like the United States.

Dual Fuel Fracturing: At the Crossroads of Technology and Sustainability

Fracturing dual fuel engine systems are reshaping how oilfield operators approach environmental goals, fuel costs, and operational efficiency. By enabling the use of readily available field gas alongside diesel, these systems reduce dependency on conventional fuels while lowering emissions and cutting costs by up to 70%.

“Dual fuel engines aren’t just a trend, they’re a strategic bridge toward cleaner oilfield operations,” said a lead analyst at Precedence Research. “They’re especially important in an energy transition period where reliability and emissions reduction must coexist.

Shale Gas Renaissance and The U.S. Dominance”

North America, particularly the United States, remains the undisputed epicenter of the market. With the U.S. Energy Information Administration (EIA) forecasting shale production to keep rising, demand for next-gen fracturing systems is at an all-time high. In 2024, North America accounted for over 38.1% of the global market share.

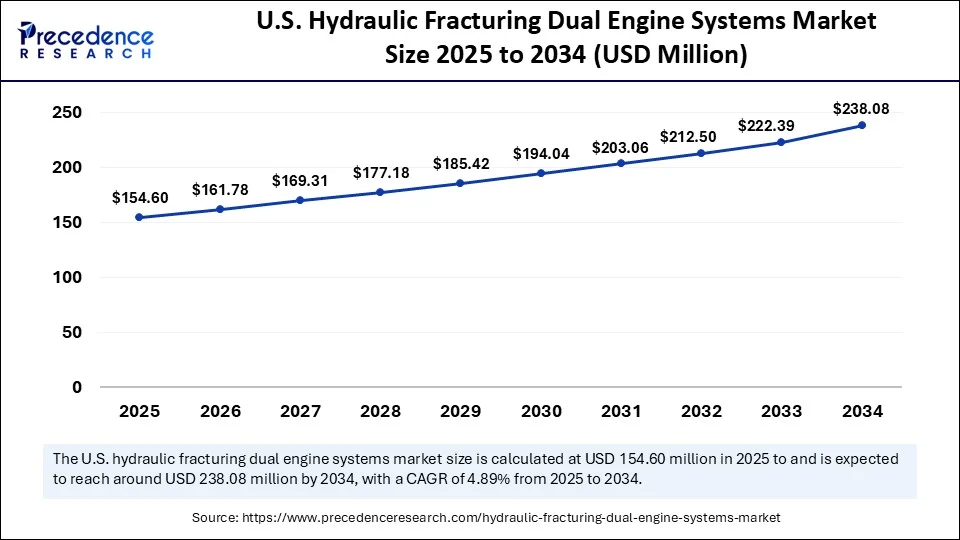

U.S. Hydraulic Fracturing Dual Engine Systems Market Size

The U.S. hydraulic fracturing dual engine systems market size was exhibited at USD 147.73 million in 2024 and is projected to be worth around USD 238.08 million by 2034, growing at a CAGR of 4.89% from 2025 to 2034.

Key contributors include the Permian Basin, Eagle Ford, and Marcellus Shale regions, where dual fuel fleets are rapidly replacing traditional diesel engines. Government incentives for methane reduction and the growing availability of field gas further boost regional adoption.

Segmental Insights: A Deeper Look Into the Market’s Backbone

Engine Type Analysis

Natural Gas Engines – Market Leader

Natural gas engines are the preferred choice for modern fracking operations due to their ability to utilize field gas or compressed natural gas (CNG) as the primary fuel source. These engines help reduce diesel consumption by 60%–80%, significantly lowering operational expenses and carbon emissions. Their high thermal efficiency and low particulate output make them ideal for shale-rich regions like the Permian Basin and Eagle Ford.

Key Benefits:

- Reduced greenhouse gas emissions (notably CO₂ and NOx)

- Better alignment with carbon credit policies

- Lower fuel costs in regions with abundant gas supply

Diesel Engines – Traditional, But Declining

Diesel-only engines, once dominant in hydraulic fracturing, are gradually losing ground. However, they continue to play a role in regions lacking gas infrastructure or where cost of conversion is prohibitive. Diesel engines are also favored in emergency backup or remote basin operations.

Challenges:

- High fuel cost volatility

- Emissions compliance burdens

- Limited future scalability in eco-sensitive zones

Others – Hybrid & Bi-Fuel Systems

Emerging engine configurations combining battery packs, hydrogen blending, or advanced biofuels are currently in the R&D and pilot testing phases. These technologies show promise in off-grid fracturing, particularly in offshore environments and exploratory drilling where environmental scrutiny is highest.

Technology Analysis

Dedicated Dual-Fuel Engines – Performance-Focused

These systems are purpose-built to run simultaneously on diesel and natural gas with sophisticated fuel injection control. They are factory-installed, designed for high-volume, high-pressure pumping, and feature advanced fuel mapping systems to optimize efficiency under variable load.

Use Cases:

- Deployed by Tier-1 oilfield service providers

- Ideal for continuous fracking operations requiring high uptime

- Integrated with emissions analytics software

Retrofit Kits – Cost-Effective and Rapidly Expanding

Retrofit kits allow existing diesel engines to be modified for dual-fuel functionality, offering a fast-track approach to sustainability for mid-sized operators. These kits are modular, relatively low-cost, and can be installed on-site with minimal operational disruption.

Growth Drivers:

- Lower upfront investment vs. new systems

- Strong appeal in developing markets (Asia, Latin America)

- Ideal for companies under capex constraints

Others – Control Units, Emission Sensors & IoT Integration

This category includes innovations such as real-time emission tracking, telemetry-enabled diagnostics, and automated fuel mixing systems. These technologies provide data-driven insights to improve fuel economy and regulatory compliance.

Noteworthy Trend:

Integration with oilfield IoT platforms and SCADA systems is accelerating the adoption of smart dual-fuel engines.

Application Analysis

Onshore Operations – Dominant Segment

Onshore shale fields represent over 85% of global hydraulic fracturing activity, making them the primary market for dual-fuel engine systems. Regions like North America, China, and parts of the Middle East are investing heavily in dual-fuel fleets for sustainable expansion.

Key Factors:

- Easy access to natural gas pipelines or flare gas

- Growing demand for eco-efficient fracking equipment

- High return on investment through fuel savings and ESG alignment

Offshore Operations – Niche but Rising

Offshore fracturing, while smaller in scope, is gaining attention due to environmental regulations in Gulf of Mexico, North Sea, and Brazilian deepwater basins. Dual-fuel systems in offshore rigs help reduce onboard diesel storage and offer real-time emissions control in sensitive ecosystems.

Challenges:

- Space constraints for gas storage

- High integration complexity with marine power systems

- Requires more stringent equipment certification

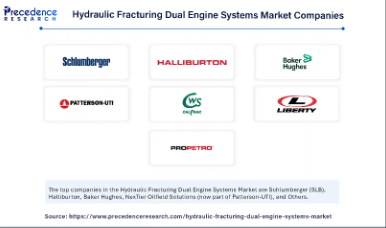

Hydraulic Fracturing Dual Engine Systems Market Key Players

Schlumberger (SLB)

Halliburton

Baker Hughes

NexTier Oilfield Solutions (now part of Patterson-UTI)

Calfrac Well Services

Liberty Oilfield Services

ProPetro Holding Corp.

combined with superior switching performance")

{kind=link}