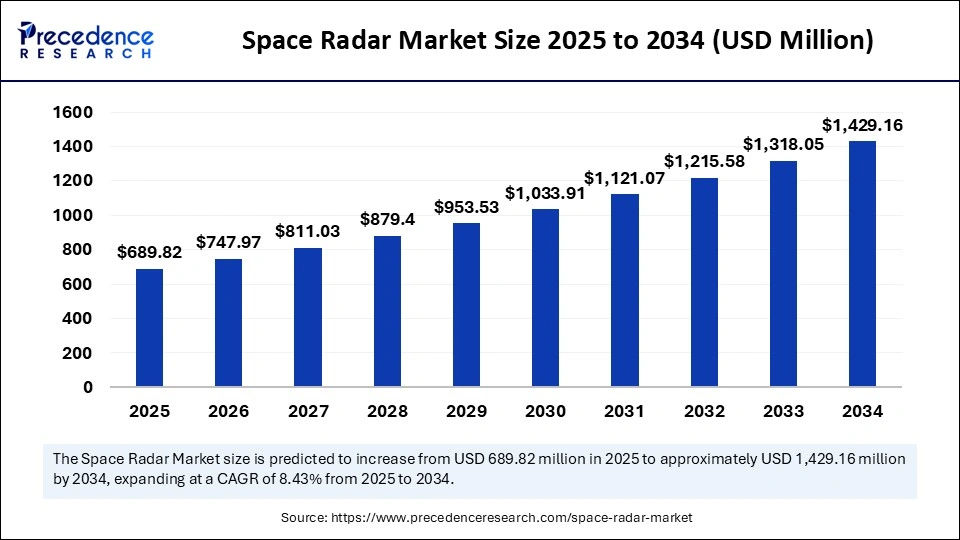

The global space radar market size is estimated to reach around USD 1,429.16 million by 2034 increasing from USD 636.19 million in 2024, with a CAGR of 8.43%.

Market Overview

The global Space Radar Market is undergoing significant expansion, fueled by the growing demand for advanced surveillance, earth observation, and real-time monitoring capabilities. Space-based radar systems, particularly those using Synthetic Aperture Radar (SAR), play a vital role in collecting high-resolution imagery and data from orbit. These systems are indispensable for a wide range of applications, including environmental monitoring, military intelligence, disaster management, and infrastructure development.

Unlike optical sensors, space radar technologies can operate in all weather conditions and during both day and night, making them uniquely valuable in time-sensitive or low-visibility scenarios. Government agencies, defense organizations, and private satellite operators are increasingly adopting radar-equipped satellites to address both national security priorities and global challenges like climate change and natural disaster response. With the miniaturization of radar sensors and a surge in low-Earth orbit (LEO) satellite constellations, the commercial side of the market is also gaining momentum, creating new revenue opportunities in sectors such as agriculture, maritime tracking, and urban planning.

Growth Factors Driving the Market

A primary growth engine behind the space radar industry is the adoption of SAR technology. SAR offers high-resolution, all-weather, and day-night imaging capabilities critical for defense reconnaissance, disaster response, monitoring environmental changes, agriculture, and infrastructure planning. In 2023, SAR comprised over 60% of the space radar market share. Another major growth driver is the surge in earth observation applications; this functional area held over 40% of market revenue in 2023 . Organizations rely on radar satellites for real-time monitoring of climate patterns, natural disasters, deforestation, ice melt, and maritime activity making space radar indispensable in the data economy.

Military applications also play a significant role. The ongoing Russia Ukraine war, for example, has underscored the importance of space-based missile tracking and intelligence gathering. The conflict has spurred increased investment in radar-equipped satellites for surveillance and security. Moreover, global tensions have accelerated demand for space situational awareness and space debris monitoring, as satellite constellation deployments proliferate.

Regional Insights

North America leads the global space radar market, holding the largest regional share in 2023. The U.S. has a developed space infrastructure, led by NASA, the DoD, and commercial entities like SpaceX and Capella Space all of which support frontier radar missions. Capella Space secured a USD 15 million U.S. Air Force contract in September 2024 for SAR satellites tailored to military intelligence.

Europe also offers a well-established presence, led by ESA’s Copernicus program and the NISAR collaboration between NASA and ISRO. EU nations are investing in multi-agency satellite constellations that include radar sensors for geospatial and climate monitoring.

In the Asia-Pacific, countries like China, India, Japan, and South Korea are making rapid progress in space radar technologies. China and India are pursuing autonomous SAR missions; India is pioneering domestically produced space radar solutions under Make-in-India initiatives.

Emerging players include Latin America (e.g., Brazil and Argentina) and the Middle East & Africa, where governments are investing in space for environmental monitoring, security, and communications

Market Drivers

Defense & Security Needs: Heightened global tensions and testaments, like the Ukraine conflict, underscore space assets’ critical role in national security. Space radars enhance ISR (intelligence, surveillance, reconnaissance) capabilities and missile detection.

Environmental and Disaster Monitoring: Growing extreme weather events necessitate radar satellites for real-time observations and disaster response support. This role is critical in UN and government climate efforts.

Commercial Satellite Proliferation: The miniaturization of SAR sensors has enabled small satellite deployments by commercial firms like Capella Space, offering more frequent data refresh cycles.

Space Pollution Management: Tracking orbital debris and preventing satellite collisions is now essential. Radar systems are integral to Space Situational Awareness (SSA) architectures.

Technological Synergy: Advances in digital beamforming, AI-enhanced data analytics, and miniaturized SAR payloads are pushing technological frontiers.

Opportunities in the Space Radar Market

The disaster management and climate monitoring segment holds substantial promise, as SAR systems can visualize earth surface changes, flooding, ice cover, and land-use dynamics. Data from these systems are becoming part of global environmental policy frameworks.

Defense-related contracts such as Capella’s government deals—highlight commercial potential in military markets. Smaller and more frequent SAR missions provide valuable data for tactical military applications.

Cross-sector partnerships offer another growth avenue. Collaborations between satellite operators and analytics firms (e.g., Capella with SATIM) are delivering enhanced intelligence services across agriculture, infrastructure, and environment domains.

Developments in digital beamforming and MIMO radar systems offer improved resolution and processing capabilities, enabling multi-modal platforms with variable frequencies and resolutions.

Space debris tracking also opens a high-growth niche. With orbital traffic surging, demand is rising for real-time debris surveillance and collision avoidance technologies.

Market Challenges & Risks

High Development & Deployment Costs: Building and launching radar satellites remains expensive—requiring advanced materials, sensitive instrumentation, and reliable launch systems. These costs limit smaller economies’ engagement.

Technical Complexity and Integration: Deploying SAR systems and integrating them within existing space missions requires specialist expertise. Adding digital beamforming and AI analytics increases complexity and project risk.

Regulatory Barriers and Export Controls: Dual-use nature of radar technology often triggers rigorous export regulation, especially for defense applications. These legal barriers can complicate international coordination and technology sharing.

Data Management Challenges: High-resolution radar satellites produce massive data volumes, requiring fast storage, transmission, and processing solutions. Ensuring secure and efficient data channels is essential.

Geopolitical Considerations: Radar satellites’ defense utility is sensitive; data sovereignty concerns may hinder cross-border data sharing and collaboration.

Recent Developments

In May 2025, India continues to strengthen its Earth observation and radar satellite capabilities through high-profile international collaborations and climate-focused missions. ISRO Chairman Dr. V. Narayanan announced the scheduled launch of the much-anticipated NASA-ISRO Synthetic Aperture Radar (NISAR) mission. This satellite carries two advanced payloads—one developed by NASA and the other by ISRO—designed for detailed microwave remote sensing. NISAR is expected to monitor Earth’s surface deformation and ecosystem disturbances with unprecedented accuracy, supporting disaster response, agricultural planning, and environmental research.

In May 2025, Japan’s commercial space radar segment gained momentum in 2025 through targeted satellite deployments and a strategic constellation roadmap. The launch placed the payload into a 575-kilometer circular orbit with a 42-degree inclination, enhancing the company’s imaging capabilities. QPS-SAR-10 is the tenth satellite launched by iQPS, marking its continued progress despite earlier setbacks, including launch vehicle failures in 2022. iQPS aims to expand its constellation to 24 satellites by 2027 and ultimately to 36, offering frequent revisit times and high-resolution radar imaging for urban infrastructure analysis, disaster monitoring, and maritime awareness.

In November 2024, China is rapidly scaling its state-directed radar satellite operations to support national mapping, surveillance, and environmental objectives. The China Aerospace Science and Technology Corporation (CASC), through its subsidiary Shanghai Academy of Spaceflight Technology (SAST), launched two radar-equipped satellites—SuperView Neo-2 03 and 04—onboard a Long March 2C rocket from Jiuquan Satellite Launch Center. The strategic expansion of China Siwei’s SAR infrastructure showcases the nation’s continued investment in dual-use technologies that support both economic planning and national security initiatives, further intensifying regional competition in orbital radar systems.

Space Radar Market Key Players

- AIRBUS

- BAE Systems

- Boeing

- Capella Space

- Denel Dynamics

- ICEYE

- Leonardo S.p.A.

- Lockheed Martin Corporation

- NEC Corporation

- Northrop Grumman

- RTX

- Saab AB

- Thales

combined with superior switching performance")

{kind=link}