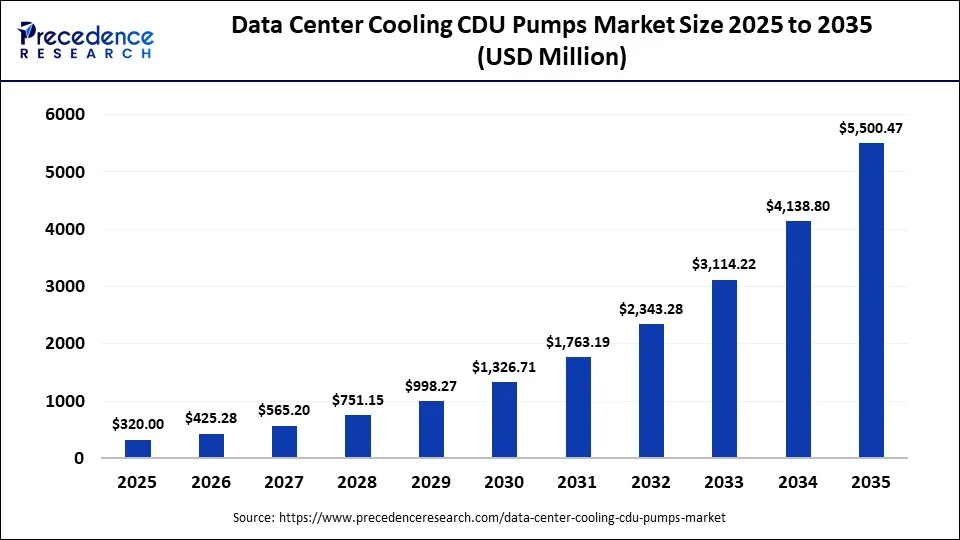

The global Data Center Cooling CDU Pumps Market is entering a transformative growth phase as artificial intelligence (AI), cloud computing, and high-performance computing (HPC) continue to increase demand for high-density data center infrastructure. According to Precedence Research, the global data center cooling CDU pumps market size was valued at USD 320 million in 2025 and is projected to grow from USD 425.28 million in 2026 to approximately USD 5.50 billion by 2035, registering a remarkable CAGR of 32.90% during the forecast period.

The accelerating digital transformation of enterprises, rapid expansion of hyperscale data centers, and unprecedented investments in AI infrastructure are driving demand for advanced coolant distribution unit (CDU) pump systems that deliver efficient and reliable liquid cooling. As next-generation processors and AI accelerators generate significantly higher thermal loads, data center operators are increasingly adopting liquid cooling solutions to enhance operational efficiency, reduce energy consumption, and improve equipment longevity.

CDU pumps have become an essential component of modern thermal management systems by regulating coolant flow, temperature, and pressure throughout servers, GPUs, and storage infrastructure. Their ability to support higher rack power densities while reducing thermal stress is making them indispensable in AI-focused computing environments.

Artificial Intelligence Reshapes Cooling Infrastructure

Artificial intelligence has emerged as one of the strongest catalysts for innovation in data center cooling technologies. AI workloads require significantly greater computing power than traditional enterprise applications, resulting in higher heat generation and increased cooling requirements.

Modern CDU pump systems enable scalable liquid cooling architectures capable of supporting AI clusters and high-performance computing environments while maintaining energy efficiency and operational reliability. Their precision cooling capabilities help extend hardware lifespan, reduce maintenance requirements, and ensure continuous system performance even under intensive workloads.

As organizations continue investing in AI-powered services and machine learning infrastructure, advanced cooling technologies are expected to become a strategic priority across enterprise, hyperscale, and colocation facilities.

Liquid Cooling Continues to Dominate Market Adoption

Liquid cooling maintained its leadership position in 2025, accounting for 63% of the global market as organizations increasingly shift away from conventional air-based cooling systems. The technology offers superior thermal efficiency, lower power usage effectiveness (PUE), and improved sustainability, making it particularly suitable for AI servers and GPU-intensive applications.

Industry investments are also accelerating in advanced cooling technologies such as direct-to-chip cooling, immersion cooling, and liquid-to-liquid CDU systems that enable operators to support higher computing densities while minimizing energy consumption.

Hybrid cooling solutions continue gaining traction among operators modernizing legacy infrastructure, while air-assisted liquid cooling is projected to witness one of the fastest growth rates throughout the forecast period due to its flexibility and simplified deployment.

Rack-Level CDU Systems Lead Infrastructure Deployment

Rack CDU solutions represented the largest share of the market in 2025 as rack-level liquid cooling becomes increasingly common across AI deployments. These compact cooling systems simplify installation while providing localized thermal management for high-density server environments.

Meanwhile, modular CDU platforms are expected to record the fastest growth through 2035, driven by increasing adoption of prefabricated and modular data centers. Their plug-and-play architecture, reduced installation complexity, and scalability make them particularly attractive for rapidly expanding AI infrastructure projects.

Centrifugal Pumps Remain the Preferred Technology

Centrifugal pumps accounted for more than 60% of global revenue in 2025 due to their high hydraulic efficiency, operational reliability, and widespread compatibility with liquid cooling systems.

At the same time, magnetic drive pumps are witnessing accelerated adoption because of their leak-free operation and maintenance-free design. Their ability to safely circulate dielectric coolants is making them increasingly valuable for next-generation AI and HPC deployments where system reliability is paramount.

AI Computing Drives Application Growth

Among applications, AI computing generated the highest market revenue in 2025 and is projected to remain the fastest-growing segment throughout the forecast period.

The rapid deployment of AI accelerators, GPU clusters, and machine learning infrastructure has significantly increased cooling requirements across hyperscale data centers. Cloud computing and HPC applications continue contributing substantial demand as service providers expand digital infrastructure to support enterprise digital transformation initiatives worldwide.

Cloud service providers remain the largest end-user category, supported by continued investments in hyperscale facilities and energy-efficient infrastructure. Healthcare is expected to emerge as one of the fastest-growing end-user industries as AI-assisted diagnostics, medical research, and data-intensive healthcare applications require precision cooling solutions for mission-critical computing environments.

North America Maintains Leadership While Asia-Pacific Accelerates

North America accounted for 39% of the global market in 2025, supported by early adoption of advanced liquid cooling technologies, strong hyperscale data center investments, and expanding AI infrastructure across the United States.

The U.S. continues to lead regional growth owing to its concentration of hyperscale cloud providers, advanced semiconductor ecosystem, and rapid deployment of AI-focused computing facilities.

Asia-Pacific is expected to register the fastest growth over the next decade as countries including China, India, Japan, Singapore, and South Korea significantly expand digital infrastructure. Government-backed digitalization initiatives, semiconductor investments, and AI development programs continue to strengthen the region’s long-term market outlook.

Europe also remains an important growth market, where sustainability regulations, energy-efficiency targets, and digital sovereignty initiatives are encouraging adoption of next-generation liquid cooling infrastructure.

Industry Innovation Accelerates

Technology providers continue introducing new CDU platforms designed specifically for AI and high-density computing environments.

Recent product launches include enterprise-grade coolant distribution units capable of supporting cooling capacities exceeding 2 MW, alongside modular HVAC and liquid cooling systems engineered for hyperscale and colocation facilities. These innovations reflect the industry’s focus on improving thermal efficiency, scalability, and operational resilience as AI infrastructure expands globally.

Competitive Landscape

The market remains semi-consolidated, with leading manufacturers focusing on product innovation, energy-efficient pump technologies, modular cooling architectures, and strategic collaborations with hyperscale operators and infrastructure providers.

Major Companies Operating in the global Data Center Cooling CDU Pumps Market

- Grundfos Holding A/S: Grundfos Holding A/S offers high-efficiency centrifugal pumps, inline pumps, end-suction pumps, and variable-speed pumping systems for data center liquid cooling applications. Its portfolio also includes intelligent pump controls, digital monitoring solutions, and integrated pumping systems designed to improve the performance and energy efficiency of Coolant Distribution Units (CDUs).

- Xylem Inc.: Xylem Inc. provides Bell & Gossett circulation pumps, vertical inline pumps, end-suction pumps, and smart pumping solutions for chilled water and liquid cooling systems. The company also offers intelligent controls and monitoring technologies that support efficient coolant circulation in data center CDUs.

- WILO SE: WILO SE offers high-efficiency ECM circulation pumps, multistage pumps, booster systems, and IoT-enabled smart pumping solutions for precision cooling applications. Its products are designed to ensure reliable coolant circulation and optimized energy consumption in data center cooling infrastructure.

- EBARA Corporation: EBARA Corporation supplies stainless steel centrifugal pumps, inline pumps, end-suction pumps, and vertical multistage pumps for industrial cooling systems. These solutions are widely used in data center liquid cooling applications, providing dependable coolant circulation for CDU and chilled water systems.

- Flowserve Corporation: Flowserve Corporation offers engineered centrifugal pumps, vertical turbine pumps, mechanical seals, and pump automation solutions for mission-critical cooling systems. Its high-reliability pumping technologies support continuous coolant circulation in hyperscale and enterprise data center cooling applications.

- Johnson Electric Holdings Limited: Johnson Electric Holdings Limited provides brushless DC motors, electronically commutated (EC) motors, integrated motor drives, and compact coolant circulation pump technologies. These components are commonly integrated into CDU pump assemblies and advanced liquid cooling systems for high-density data centers.

- Panasonic Holdings Corporation: Panasonic Holdings Corporation offers brushless DC motors, electric coolant circulation pumps, electronic control modules, and thermal management components. Its technologies support compact and energy-efficient liquid cooling systems used in modern data center CDUs.

- AMETEK, Inc.: AMETEK, Inc. provides precision electric motors, motion control systems, pressure sensors, electronic controllers, and fluid management components. These products enhance the monitoring, control, and operational efficiency of CDU pumping systems in liquid-cooled data centers.

- Gates Corporation: Gates Corporation offers industrial coolant hoses, thermal transfer hoses, quick-connect fluid transfer systems, flexible tubing, and sealing solutions. These products enable reliable coolant transport and leak-resistant fluid management within CDU and liquid cooling infrastructures.

- Gorman-Rupp Industries (GRI): Gorman-Rupp Industries (GRI) manufactures magnetic drive pumps, centrifugal pumps, self-priming pumps, and compact coolant circulation systems. Its pumping solutions are designed for efficient liquid transfer and thermal management in data center cooling applications.

- SPP Pumps Limited: SPP Pumps Limited provides split-case pumps, end-suction pumps, vertical turbine pumps, and booster pumping systems for large-scale cooling networks. Its engineered water circulation solutions support the cooling requirements of hyperscale and enterprise data centers.

- Speck Group: Speck Group offers high-performance centrifugal pumps, regenerative turbine pumps, immersion cooling pumps, and customized coolant circulation systems. Its pump technologies are specifically developed for liquid cooling applications, including CDU and immersion-cooled data center environments.

- SPAL Automotive Srl: SPAL Automotive Srl manufactures brushless electric coolant pumps, DC water pumps, and EC motor-based circulation systems. These compact and energy-efficient products are suitable for electronics cooling and liquid-cooled data center applications.

- GuangDong Shenpeng Technology Co., Ltd.: GuangDong Shenpeng Technology Co., Ltd. specializes in DC brushless water pumps, miniature coolant pumps, electronically controlled circulation pumps, and OEM liquid cooling pump modules. Its products are widely used in AI servers, CDUs, and electronic thermal management systems.

- Changsha TOPS Industry & Technology Co., Ltd.: Changsha TOPS Industry & Technology Co., Ltd. offers magnetic drive centrifugal pumps, DC coolant pumps, high-pressure circulation pumps, and customized liquid cooling pump assemblies. Its solutions are designed to support efficient coolant flow in data center CDUs, industrial cooling systems, and other precision thermal management applications.

As AI adoption continues to reshape global computing infrastructure, demand for advanced liquid cooling solutions is expected to accelerate substantially over the next decade. CDU pump technologies are poised to play a central role in enabling sustainable, energy-efficient, and high-performance data center operations capable of supporting the next generation of digital innovation.

combined with superior switching performance")

{kind=link}