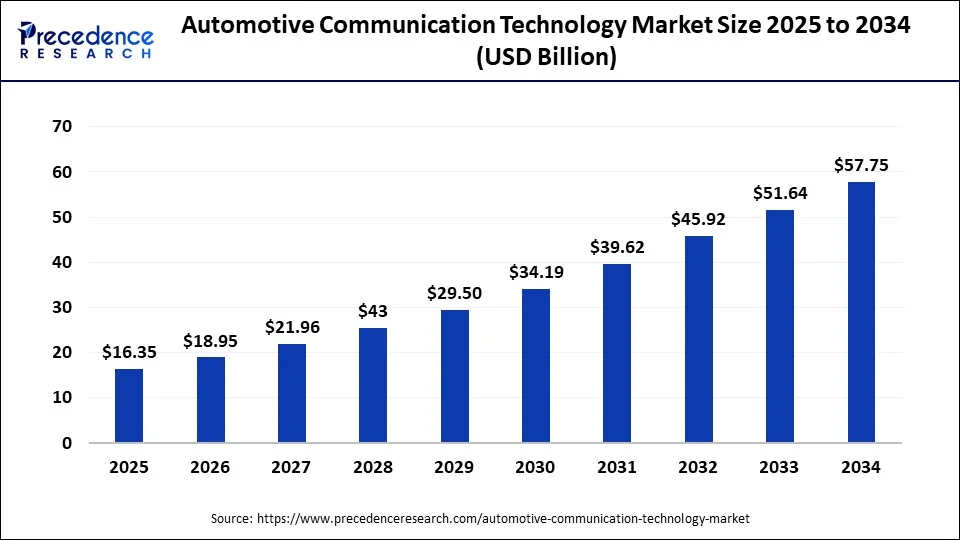

The global automotive communication technology market is set for explosive growth, projected to reach USD 57.75 billion by 2034, expanding at a robust CAGR of 15.14% from 2025 to 2034.

Propelled by the adoption of smart vehicles, electric cars, and advanced driver assistance systems (ADAS), the automotive communication technology market reached USD 14.10 billion in 2024 and is forecasted to reach USD 57.75 billion by 2034, riding a CAGR of 15.14%. Dominance in this sector is largely due to rising demand for connectivity, safety, and miniaturization of electronics in vehicles worldwide.

Automotive Communication Technology Market Key Insights

- The global market hit USD 14.10 billion in 2024; expected to reach USD 57.75 billion by 2034.

- Asia Pacific accounts for 44.7% of 2024’s market share and is projected to maintain its leadership.

- CAN bus module commanded a 38.7% revenue share in 2022.

- Ethernet technology is lagging but anticipated to grow the fastest at 20.87% CAGR.

- Mid-size vehicles captured the largest revenue share in 2023; luxury cars see burgeoning growth.

- Body control & comfort applications generated $2.62 billion revenue in 2023 due to safety and luxury demand.

Revenue Table

| Metric | Value |

|---|---|

| Market Size (2024) | USD 14.10 Billion |

| Market Size (2025) | USD 16.35 Billion |

| Market Size (2034) | USD 57.75 Billion |

| Largest Region (2024) | Asia Pacific |

| Asia Pacific Market Size (2025) | USD 5.72 Billion |

| Asia Pacific Market Size (2034) | USD 20.21 Billion |

How is AI Reshaping Automotive Communication Technology?

AI drives smarter, safer vehicles: Artificial intelligence is a backbone for connected car solutions that power real-time vehicle diagnostics, predictive maintenance, and advanced safety systems like ADAS and autonomous driving platforms. Integrating AI boosts ECUs (Electronic Control Units), now with as many as 70 per modern vehicle, poised to rise to 500 in coming years—topping even space shuttles.

AI transforms in-vehicle experiences: Machine learning algorithms enhance comfort and security, offering features like facial recognition and intelligent infotainment. AI’s fusion with IoT and big data analytics ensures robust communication networks for adaptive cruise control, smart parking, and engine optimizations, making vehicles both intuitive and interactive.

What’s Driving Automotive Communication Technology’s Meteoric Growth?

- Soaring demand for autonomous and connected vehicles boosts the need for fast in-vehicle networks.

- Surge in electric vehicle (EV) uptake creates new requirements for communication modules.

- IoT’s proliferation, miniaturized chips, and declining component costs catalyze faster system upgrades.

- Stringent government safety regulations push integration of advanced telematics and safety networks.

- Customer preference shifts toward premium, feature-rich vehicles for enhanced comfort and safety.

Opportunity and Trend: Where Will the Next Big Disruption Arise?

How Will Connected Cars and EVs Shape Market Opportunities?

The transition to connected vehicles and electric mobility continues to create lucrative opportunities for innovation, especially as manufacturers invest in strategic alliances, develop novel semiconductor solutions, and leverage big data analytics.

Regional Momentum: The Asia Pacific Powerhouse

Asia Pacific leads as the automotive epicenter, accounting for 45% of market share in 2024, with strong outlook based on robust automotive manufacturing and rapid EV adoption.

North America notably advances in autonomous vehicles and ADAS, driven by strict regulations and infrastructure. Latin America and Middle East & Africa showcase high growth potential due to untapped consumer bases and increased tech investments.

Market Segmentation Analysis

By Bus Module

Controller Area Network (CAN): Dominates with 38.7% share in 2022 and remains the preferred module due to broad application across vehicles and ease of integration with IoT, autonomous driving, and enhanced vehicle functionality.

Local Interconnect Network (LIN): Widely used for cost-effective communication in simpler functions, such as body electronics.

Media-Oriented Systems Transport (MOST): Specialized for infotainment and multimedia networking within vehicles.

FlexRay: Applied for high-speed, safety-critical automotive systems, favored in ADAS and autonomous platforms.

Ethernet: Fastest-growing segment, projected at a 20.87% CAGR, catering to new applications needing ultra-fast data transfer such as adaptive cruise control and smart parking.

By Application

Body Control & Comfort: Largest segment with USD 2.62 billion revenue in 2023, driven by rising safety standards and luxury comfort features.

Powertrain: Expected exponential growth as the need for secure, smooth driving and high-efficiency engines intensifies, particularly with new government policies aimed at reducing emissions.

By Vehicle Class

Mid-size vehicles: Captured most of the market revenue in 2023, remaining the choice for most consumers due to affordable pricing and comprehensive feature sets that enhance comfort and accessibility.

Luxury vehicles: Set to rise rapidly in market share, propelled by a growing global middle class and increased purchasing power, with heightened demand for premium, technologically sophisticated vehicles.

Latest Breakthroughs

- Toshiba America Electronic Components Inc.: Launched TC9562 series with advanced ethernet capability for infotainment & telematics systems.

- Autohome Inc.: Invested in TTP Car Inc., spurring China’s used car auction market.

- Other unnamed top giants focus on strategic alliances, R&D, and semiconductor innovations for next-gen automotive solutions.

Automotive Communication Technology Market Companies

Toshiba Corporation

- Focuses on semiconductor innovations for electrification, battery management, and motor control, plus RF-ICs for wireless automotive communication.

- Offers CXPI-compliant communication ICs for applications such as steering and instrument clusters, and bridges analog/digital interfaces.

Robert Bosch GmbH

- A global leader in powertrain, safety, infotainment, and networking solutions.

- Active in developing automotive Ethernet and new ECUs for digital cockpits, ADAS, and emission control, with constant expansion and innovation partnerships.

- Invests heavily in R&D for connected mobility, autonomous driving, and sustainability.

Texas Instruments

- Supplies automotive-grade transceivers, processors, and DLP infotainment/lighting technology, enabling robust in-vehicle networking.

- Designs solutions for high-speed and reliable communication in electric and autonomous vehicles.

Broadcom Inc.

- Pioneers automotive Ethernet (BroadR-Reach), enabling high-bandwidth data over lightweight cabling for infotainment and ADAS.

- Founding member of OPEN Alliance, driving Ethernet adoption as a vehicle networking standard.

NXP Semiconductors

- World leader in secure, mixed-signal connectivity for safety-critical functions, sensor systems, short-range high-speed communication, and in-vehicle networking.

- Active in V2X, ADAS, and processing technologies for autonomous and connected cars.

Infineon Technologies AG

- Supplies microcontrollers, safety ICs, sensors, and power devices for ADAS, body electronics, and EV powertrains.

- Focus on vehicle safety, LED lighting, EV management, and infotainment networking.

STMicroelectronics

- Develops MCUs for networking, especially for next-gen architectures, with Arm®-based Stellar series offering broad protocol support, security, and infotainment integration.

Renesas Electronics Corporation

- Specializes in gateway SoCs for next-gen E/E architectures, prioritizing power efficiency, secure communication, and high-speed networking for cloud-connected vehicles.

Microchip Technology Inc.

- Provides automotive-grade networking ICs (CAN, LIN, Ethernet), supporting reliable, scalable communication across vehicle domains.

ON Semiconductor, Rohm Semiconductor, Maxim Integrated, Melexis NV, Elmos Semiconductor SE

- Offer specialized semiconductors and sensors (e.g., for ADAS, LIN/CAN/Ethernet transceivers, power management, RF, lighting, and safety) that underpin communication infrastructure in vehicles.

Xilinx Inc., Analog Devices, Vector Informatik GmbH, Intel Corporation

- Xilinx: FPGA-based solutions for flexible, high-performance automotive networking and sensor fusion in ADAS.

- Analog Devices: Signal processing, connectivity, and sensor interfaces for networked vehicles.

- Vector Informatik: Engineering tools for protocol implementation, validation, and network simulation, supporting OEMs and suppliers.

- Intel: Provides processors and networking chips for connected vehicles, enabling edge computing and high-bandwidth communication.

Challenges and Cost Pressures: What’s the Roadblock?

Automotive communication technologies face cost pressures from chip prices, with IoT chips declining from $10 to $6 each yet integration and R&D can strain budgets. Developing regions must invest more to catch up technologically and balance affordability with advanced features. High data transmission needs for new systems like ADAS and smart parking demand costly, scalable infrastructures.

Case Study Highlight: Asia’s Leap in Used Car Tech

A recent investment by Autohome Inc. in China’s TTP Car Inc. turbocharged tech-driven growth in the used automotive market, leveraging advanced communication platforms and auction technologies for digital transformation.

combined with superior switching performance")

{kind=link}