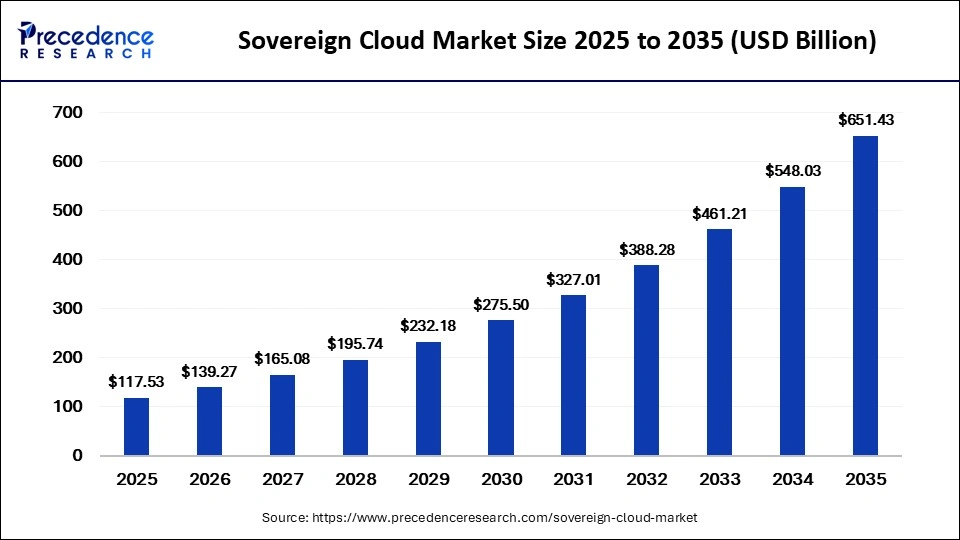

The global sovereign cloud market was valued at USD 117.53 billion in 2025 and is projected to grow to USD 139.27 billion in 2026, reaching approximately USD 651.43 billion by 2035. The market is expected to expand at a CAGR of 18.70% from 2026 to 2035, driven by the increasing enforcement of data localization regulations and the growing adoption of jurisdiction-controlled cloud infrastructure across highly regulated industries.

Key Takeaways

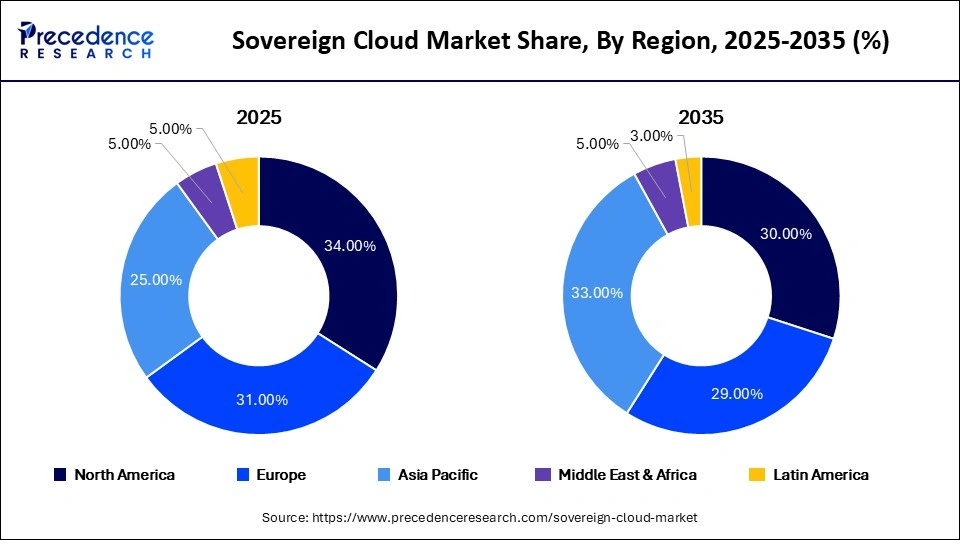

- North America dominated the sovereign cloud market with 34% of the market share in 2025.

- Asia-Pacific held the market share of 25% in 2025 and is expected to be the fastest-growing region with a CAGR of 22.1% between 2026 and 2035.

- By deployment model, the public sovereign cloud segment contributed the highest market share of 38% in 2025.

- By deployment model, the private sovereign cloud segment held the second-largest market share of 34% in 2025 and is expected to grow at a significant CAGR of 16.5% between 2026 and 2035.

- By service type, the infrastructure as a service (IaaS) segment held a major market share of 46% in 2025.

- By service type, the platform as a service segment held a 24% share of the sovereign cloud market in 2025 and is expected to register the fastest growth of 20.1% CAGR during 2026 and 2035.

Market Overview

The sovereign cloud market is experiencing significant growth due to rising government mandates focused on data sovereignty and cybersecurity resilience. Sovereign cloud refers to a cloud computing model that ensures data, operations, processes, and digital workloads remain under local jurisdiction and control within a specific region.

This approach combines hyperscale cloud infrastructure with localized governance frameworks, advanced encryption technologies, and AI processing capabilities. The market is further driven by the growing adoption of confidential computing, sovereign AI models, and national cybersecurity strategies. These factors are expected to remain key drivers of market expansion in the coming years.

Impact of Artificial Intelligence on the Sovereign Cloud Market

Artificial Intelligence (AI) is playing a significant role in the breakthrough and enhancement of infrastructures across the market. AI workloads are becoming a popular option that governments and regulated industries use to ensure jurisdictional control of sensitive data, algorithms, and digital operations in the sovereign cloud. Demand for localized hyperscale computing infrastructure and sovereign GPU clusters is growing, driven by the growing usage of Generative AI, national language models, and AI-powered analytics.

Regional Outlook of the Sovereign Cloud Market

North America

North America dominated the sovereign cloud market with a major share of 43% in 2025, due to its increasing federal cybersecurity modernization efforts. This continued to expand cloud platforms under jurisdiction, in defense, intelligence, healthcare, and financial sectors.

During 2025, the U.S. Department of Defense continued seeing deployments of JWCC across multi-cloud scenarios, bolstering its capability to distribute workloads across the U.S. sovereign. FedRAMP reported over 400 cloud services, and it has tentatively demonstrated robust interest in compliance certification among federal agencies for sovereign cloud services, thus further fueling the regional market growth.

Asia Pacific

Asia-Pacific held a 25% share of the market in 2025 and is expected to be the fastest-growing region with a CAGR of 22.1% between 2026 and 2035, driven by fast enterprise cloud adoption across China, India, Japan, and South Korea/Southeast Asia. Deployment of localized digital infrastructure is gaining pace.

Soaring investment in programs of smart cities, digital banking technology, and AI-based public services also enhanced long-term demand for sovereign clouds. Regional infrastructure scalability was helped by the growth of domestic semiconductor ecosystems and investments in data center power using renewables.

Europe

Europe held the second-largest market share of 31% in 2025 and is expected to grow at a CAGR of 17.9% over the projected period, supported by strong long-term growth through expanding regional sovereignty initiatives. Compliance with GDPR and new data residency regulations around the region pushed enterprises to consider shifting critical applications to European data centers and cloud services. The long-term strategic value of Europe’s cloud value increased even more as new demands for industrial AI and secure digital public services continued to grow across jurisdiction-controlled environments.

Sovereign Cloud Market Companies

Microsoft

Microsoft generated USD 281.7 billion in revenue in FY2025 and is a leading provider of sovereign cloud solutions through Microsoft Cloud for Sovereignty, enabling governments and regulated industries to maintain data residency, compliance, and operational control. The company leverages its Azure infrastructure, AI capabilities, and advanced security services to support national digital sovereignty initiatives worldwide.

Amazon Web Services (AWS)

AWS recorded an annual revenue run rate of approximately USD 142 billion in 2025, maintaining its position as the world’s largest cloud provider. The company offers sovereign cloud and digital sovereignty solutions that help public-sector organizations and regulated enterprises meet data localization, security, and compliance requirements.

Google Cloud

Google Cloud achieved an annual revenue run rate of approximately USD 71 billion in 2025 and continues to expand its sovereign cloud portfolio. Its offerings focus on data sovereignty, confidential computing, and AI-powered cloud services, enabling organizations to retain control over sensitive data while benefiting from hyperscale cloud infrastructure.

Oracle

Oracle reported USD 57.4 billion in revenue in FY2025 and is strengthening its presence in the sovereign cloud market through Oracle Cloud Infrastructure (OCI) and dedicated sovereign cloud regions. The company’s solutions are designed to help governments and regulated sectors maintain strict control over data, applications, and compliance frameworks.

IBM

IBM generated approximately USD 62.8 billion in revenue in 2025 and offers sovereign cloud capabilities through its hybrid cloud and security-focused infrastructure. The company supports enterprises and public-sector organizations with data protection, regulatory compliance, and industry-specific cloud solutions tailored for sovereignty requirements.

SAP

SAP reported approximately EUR 21.6–21.9 billion in cloud revenue guidance for 2025 and continues to advance sovereign cloud initiatives through partnerships and localized cloud environments. Its sovereign cloud offerings help organizations comply with regional regulations while securely running mission-critical enterprise applications and data workloads.

OVHcloud

OVHcloud surpassed EUR 1.08 billion in revenue in fiscal 2025, reinforcing its position as a leading European sovereign cloud provider. The company emphasizes digital sovereignty, transparent data governance, and compliance with European regulations, making it a preferred cloud partner for governments and privacy-conscious enterprises.

Segmental Insights of the Sovereign Cloud Market

Deployment Model Insights

The public sovereign cloud segment dominated the sovereign cloud market with a share of 38% in 2025, due to the fast migration of national platforms and the growing market preference for secure infrastructure over the subscription model. Public cloud operators beefed up dedicated sovereign availability zones for region-specific compliance-governance and encrypted workload hosting of public-sector workloads.

Service Type Insights

The infrastructure as a service (IaaS) segment dominated the sovereign cloud market with a share of 46% in 2025, due to the increasing enterprise migration toward regionally governed infrastructure ecosystems. Companies in aerospace engineering, digital banking, and energy distribution sovereignty was becoming a priority in IaaS initiatives.

They focus on dedicated compute isolation and governance of infrastructure, based on jurisdiction. The OpenInfra Foundation 2025 report states production OpenStack deployments are now over 55 million documented cores, showing a growing number of cases for sovereign infrastructure requiring IaaS in the coming years.

Organization Size Insights

The large enterprises segment dominated the sovereign cloud market with a share of 71% in 2025, driven by the rapid expansion of enterprise-scale cybersecurity, data governance, and regulatory compliance initiatives. Large organizations, including multinational banks, aerospace firms, healthcare providers, and telecommunications companies, are increasingly adopting sovereign cloud solutions to maintain greater control over sensitive data, ensure compliance with data residency requirements, and secure critical operations across geographically distributed environments.

combined with superior switching performance")

{kind=link}