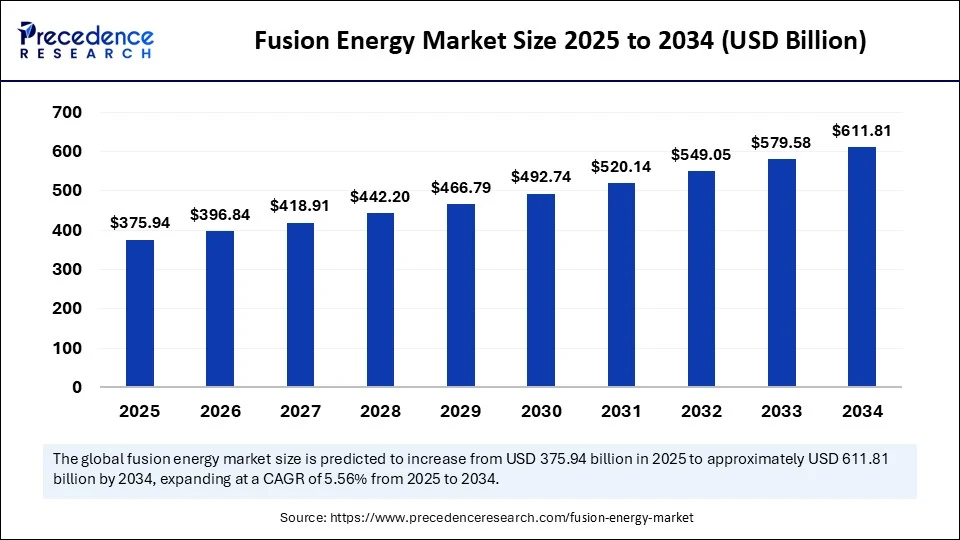

The global fusion energy market reached USD 356.14 billion in 2024 and the is expected to cross around USD 611.81 billion by 2034, growing at a CAGR of over 5.56% (Precedence Research). Driven by massive private funding and government programs, this growth reflects not only R&D investment but also the emergence of fusion pilot plants and commercial demonstration reactors.

What Is Nuclear Fusion, and How Does It Differ from Fission?

Nuclear fusion is the process of combining light atomic nuclei, typically isotopes of hydrogen, into heavier nuclei, releasing enormous energy in the process. This is the same reaction that powers our Sun and other stars.

Fusion is fundamentally different from fission, where heavy atomic nuclei (like uranium or plutonium) are split apart. While fission is the basis of today’s nuclear power plants, it produces long-lived radioactive waste and carries the risk of catastrophic failure. Fusion, on the other hand, generates no long-lived waste, is inherently safer, and does not emit CO₂.

Why Is Fusion Vital for Decarbonization?

Fusion could become the holy grail of clean energy, delivering base-load power without emissions or fuel constraints. A fusion reactor using deuterium and tritium can generate massive energy from minuscule fuel amounts, with fuel sources derived from seawater and lithium.

As the climate crisis accelerates, fusion offers a realistic route to achieving net-zero emissions by mid-century. It can complement intermittent renewables like solar and wind while reducing dependence on fossil fuels and even conventional nuclear.

What’s the Current Status of Fusion Energy?

As of 2025, fusion remains largely experimental, but the momentum is growing:

- In Europe, the ITER project in France, a multinational collaboration, is the largest experimental fusion facility in the world.

- In the U.S., national labs and startups like Helion and Commonwealth Fusion Systems (CFS) are setting aggressive commercialization targets.

- In Asia, China’s EAST reactor and Japan’s JT-60SA are making technical leaps in plasma confinement and heating.

How Exactly Does Fusion Work?

At its core, fusion requires bringing two light atomic nuclei close enough for the strong nuclear force to fuse them into one. The most promising fuel combination involves Deuterium and Tritium, both isotopes of hydrogen. Deuterium is plentiful in seawater, while tritium can be bred from lithium. Achieving fusion conditions demands extreme heat (over 100 million °C) and intense pressure, forming a plasma, a hot, electrically charged gas where electrons separate from nuclei. Two main strategies dominate this effort. The Magnetic Confinement Fusion (MCF) approach uses powerful magnets to contain plasma in donut-shaped devices called Tokamaks (e.g., ITER) or the more complex Stellarators. Alternatively, Inertial Confinement Fusion (ICF), pursued by the National Ignition Facility (NIF), compresses fuel pellets with powerful lasers. To imagine fusion, picture trying to light a miniature star and keeping it suspended inside an invisible magnetic net. It’s a physics challenge unlike any other.

What’s Behind the Fusion Momentum Since 2020?

A confluence of scientific achievement and financial backing has made 2020–2025 a watershed period for fusion. In 2021, the NIF reached a historic milestone by achieving ignition, where more energy was released than absorbed by the fuel,a key threshold for viability. Meanwhile, private-sector startups like Helion Energy, Commonwealth Fusion Systems (CFS), and TAE Technologies made major strides in plasma control, reactor design, and high-temperature superconductors. Over $6 billion in private capital has poured into fusion since 2020, signaling a shift from academic curiosity to commercial ambition. Investors and governments alike are showing growing confidence that fusion could move from theory to power plants within a generation.

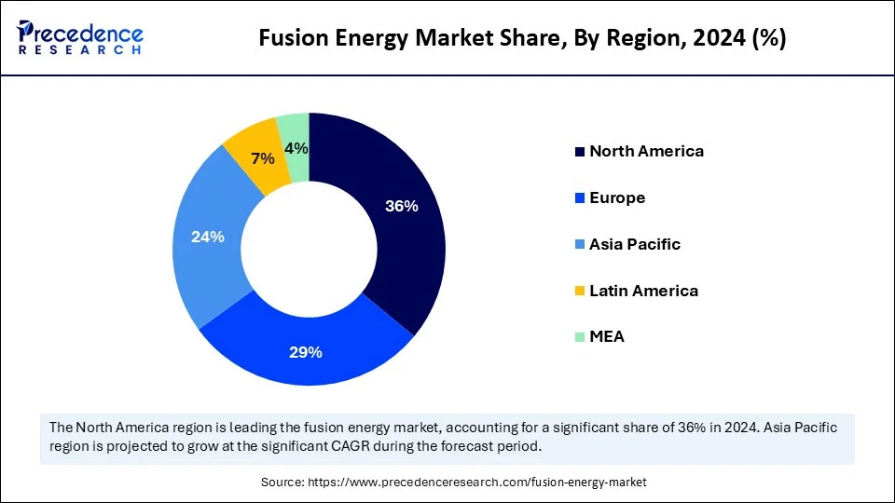

Global Powerhouses of Fusion: Who’s Advancing the Future of Clean Energy?

North America

The United States leads the charge in private fusion development, hosting a vibrant mix of pioneering startups, top-tier universities, and government-backed research. Projects like MIT’s SPARC (with Commonwealth Fusion Systems), Helion Energy, TAE Technologies, and General Atomics are setting aggressive timelines for fusion commercialization. These ventures are heavily supported by agencies like ARPA-E and the Department of Energy (DOE), which fund reactor prototyping, plasma research, and grid-readiness programs. Academic institutions like Princeton, Caltech, and MIT are key contributors to both scientific innovation and talent development.

Europe

Europe remains a cornerstone of international collaboration through the ITER project in France, the most ambitious fusion experiment ever undertaken. The EUROfusion consortium coordinates research across the continent, including the UK’s JET and upcoming DEMO reactor. In the post-Brexit era, the UK is forging its own path with the STEP fusion plant, targeting the 2040s for demonstration-scale electricity. Germany is pushing the envelope with the Wendelstein 7-X, a stellarator that offers promising plasma stability for continuous operation.

Asia-Pacific

Asia’s role in the fusion race is accelerating rapidly. China’s EAST reactor has sustained record-breaking temperatures and is being followed by the larger CFETR plant. These developments align with China’s national clean energy ambitions. Japan’s JT-60SA, built in partnership with the EU, is one of the most advanced superconducting tokamaks globally. India, a core partner in ITER, continues to expand domestic fusion capabilities via the Institute for Plasma Research (IPR) and experimental devices like SST-1 and ADITYA.

Fusion Energy Market Key Players

- Commonwealth Fusion Systems

- European Organization for Nuclear Research

- First Light Fusion

- General Fusion

- Helion Energy

- ITER Organization

- Korea Superconducting Tokamak Advanced Research

- Lawrence Livermore National Laboratory

- MAX IV Laboratory

- National Renewable Energy Laboratory

- Princeton Plasma Physics Laboratory

- Russian Federal Nuclear Center

- Tokamak Energy

- United States Department of Energy

Is Fusion Better Than Today’s Energy Sources?

Fusion’s advantages over existing energy technologies are profound. Compared to solar and wind, fusion offers consistent, on-demand power without dependence on weather. Unlike fission, fusion doesn’t risk meltdowns or create long-lived radioactive waste. And in stark contrast to fossil fuels, fusion emits no carbon dioxide and requires no mining or combustion of carbon-based resources. Economically, fusion remains expensive today, but promises significant cost reductions over time as technologies mature and scale. Safety is another key differentiator, fusion reactions are self-limiting and cannot run away uncontrollably. If containment fails, the plasma simply cools down and stops, making fusion inherently secure.

What Forces Are Driving and Shaping the Fusion Market?

The Drivers: Why Fusion Is Gaining Ground

The primary force propelling fusion is the urgent need for clean, sustainable, base-load power. As renewables struggle with intermittency and storage, fusion offers a stable and carbon-free alternative. Rising interest from venture capital and tech entrepreneurs is accelerating timelines, while new materials, such as high-temperature superconductors, are improving the feasibility of magnet-based designs. Global governments are actively supporting fusion through initiatives like ITER, ARPA-E’s BETHE program, and the UK’s STEP fusion roadmap.

The Restraints: What’s Holding Fusion Back?

Despite the promise, fusion faces enormous R&D expenses and complex engineering challenges. Managing and stabilizing plasma requires unprecedented precision and material durability, especially under sustained high-energy operation. Commercialization is still 10–20 years away for most large-scale designs, limiting near-term returns on investment and making the market heavily reliant on public funding and long-horizon capital.

The Opportunities: What Lies Ahead?

Fusion opens new avenues in hydrogen production, using reactor heat to split water molecules more efficiently. There’s also potential in AI-enhanced reactor control systems, where machine learning models predict and adjust plasma behavior in real-time. As commercial fusion scales, energy export markets in developing or power-deficient regions could unlock entirely new value chains.

Which Technologies Are Leading the Fusion Revolution?

- Fusion innovation spans several competing and complementary designs

- Tokamaks (e.g., ITER, SPARC): The most mature, though large and expensive.

- Stellarators (e.g., Wendelstein 7-X): Offer steady-state operation but with complex geometry and high cost.

- Inertial Confinement (e.g., NIF): Laser-based ignition holds promise but is currently inefficient for energy production.

- Magnetized Target Fusion (MTF): A hybrid technique where magnetic fields and mechanical compression are used—pioneered by General Fusion.

- Field-Reversed Configurations (FRC): Compact, simpler magnetic designs pursued by TAE Technologies.

Who’s Funding Fusion and What Are Their Motives?

Private capital is pouring into fusion, with heavyweights like Sam Altman (OpenAI) investing in Helion, and firms like Breakthrough Energy Ventures, Tiger Global, and Temasek backing multiple players. Startups such as CFS and TAE have raised hundreds of millions of dollars each, often in later-stage funding rounds aimed at building prototype or pilot plants. On the public side, the U.S. Department of Energy, UK Atomic Energy Authority (UKAEA), and European Commission continue to fund flagship projects. Surprisingly, even oil & gas giants like Chevron and Shell are investing in fusion, likely as a hedge against their own fossil fuel portfolios and a way to lead the transition to clean energy.

What Global Collaborations Are Pushing Fusion Forward?

Fusion research is inherently international. The ITER project involves 35 countries and is the most ambitious scientific collaboration in energy history. EUROfusion coordinates Europe’s research roadmap, while the DEMO reactor aims to be the first net electricity-producing fusion plant by the 2040s. In the U.S., ARPA-E supports a portfolio of fusion startups. Public-private partnerships, such as UKAEA’s collaborations with startups and DOE grants to Helion and CFS, are becoming more common. China’s EAST and CFETR, developed largely with domestic resources, signify a major shift toward East Asian leadership in fusion R&D.

combined with superior switching performance")

{kind=link}