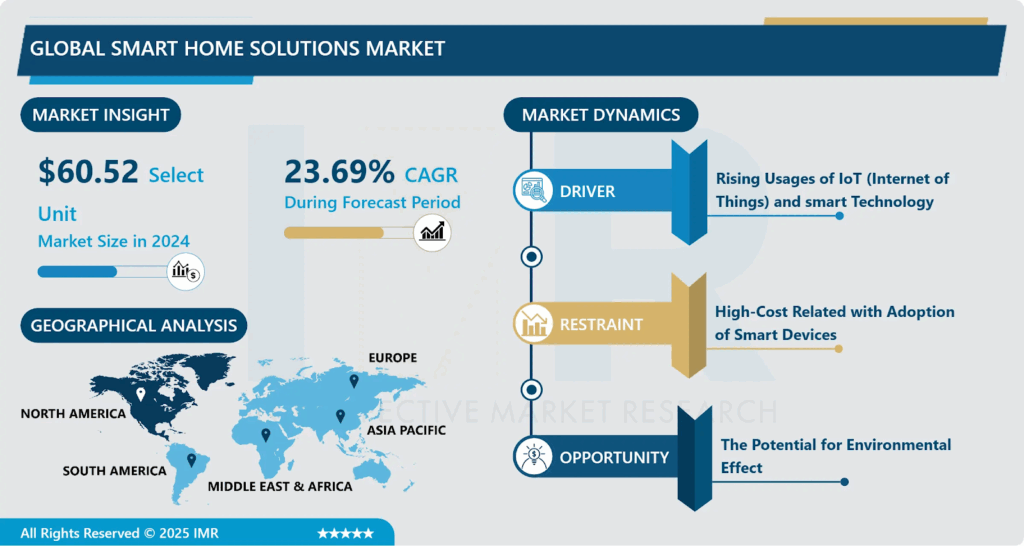

Introspective Market Research (IMR) published a major new report on the Smart Home Solutions Market, projecting a robust growth trajectory over the next decade. According to the report, the global market estimated at USD 60.52 billion in 2024 is forecast to reach USD 331.57 billion by 2032, registering a compound annual growth rate (CAGR) of approximately 23.69% between 2025 and 2032.

Driving this growth are accelerating consumer demand for energy-efficient, connected homes; increasing adoption of IoT-enabled devices; enhanced home security needs; rising disposable incomes; and the growing appeal of convenience and automation in residential living.

Quick Insights

- Market value (2024): USD 60.52 billion

- Forecast value (2032): USD 331.57 billion

- Forecast CAGR (2025–2032): ~23.69%

- Leading region (current): North America due to high consumer spending power, early tech adoption and established smart-home ecosystems

- Fastest-growing region: Asia Pacific driven by urbanization, rising middle class, growing internet penetration and increasing interest in home automation.

- Top segments: Smart security & access control; lighting control; HVAC and energy-management; home automation & entertainment ecosystems. (As per related global smart-home reports).

- Key players / brands (typical in market): Honeywell International Inc., Lutron Electronics Co., Inc., Crestron Electronics, Inc., Schneider Electric, Philips / Signify, Samsung Electronics, Nest Labs and other leading suppliers of lighting, security, HVAC and automation solutions.

What’s Fueling the Smart Home Boom?

Why are smart home solutions witnessing such strong global growth?

- Energy efficiency & cost savings: As energy costs rise and sustainability becomes more important, homeowners are gravitating toward smart lighting, HVAC control and automation to cut bills and reduce carbon footprint.

- Rise of connected living & IoT adoption: Widespread penetration of high-speed internet, smartphones, and affordable IoT devices have lowered the barrier to entry for home automation.

- Security & remote monitoring demand: Growing consumer concerns around safety, property monitoring, and peace-of-mind during travel or remote working have boosted adoption of smart security and access-control systems.

- Convenience & lifestyle upgrades: Smart lighting, voice-assisted control, entertainment integration, remote access, and seamless automation appeal to modern consumers seeking comfort and convenience.

- Urbanization & rising disposable incomes: Rapid growth of urban households, increasing incomes, and changing lifestyles particularly in Asia Pacific are pushing adoption of smart-home solutions as a lifestyle standard rather than premium add-on.

“Smart home solutions are no longer a niche luxury they are fast becoming a foundational element of residential living worldwide. As devices become more affordable, integration more seamless, and value proposition (energy savings, security, convenience) more compelling, the market is set to enter a phase of mass adoption,” says Dr. Aisha Verma, Principal Consultant, Introspective Market Research.

Regional Dynamics & Growth Projections

- North America: Continues to lead market value due to high per-household spend on smart devices, early comfort with subscription-based Smart-Home-as-a-Service models, and strong demand for security, energy efficiency and automation.

- Asia Pacific: Set to witness the highest growth rate over the forecast period, aided by expanding urban housing, rising middle-class incomes, government support for smart-city infrastructures, and growing consumer appetite for modern home technologies.

- Europe: Growth driven by energy-efficiency regulations, sustainability awareness, and mature adoption of home automation particularly for security, HVAC control and smart lighting.

- Emerging Markets (Latin America, MEA): Adoption is slower but growing steadily, especially as device prices fall, smartphone penetration rises, and income levels improve creating new opportunities for mid-range smart home solutions.

Segmentation trends suggest that security & access controls and lighting/HVAC automation will remain core growth drivers, while integrated smart-home platforms (multi-device control, AI assistants, energy-management systems) will represent the next frontier of value, particularly among premium consumers and early adopters.

Recent Innovations & Key Market Developments

- Major smart-home providers are launching integrated energy-management platforms – combining smart thermostats, lighting control, occupancy sensing and automated HVAC to optimize energy savings and carbon footprint.

- Rise of AI-enabled home assistants and voice-controlled automation from leading manufacturers – enabling seamless voice commands, scheduling, remote control and learning-based automation for lighting, security and comfort.

- Increasing availability of affordable, modular smart-home kits targeted at rental apartments and mid-income homes – lowering entry barriers for first-time adopters and fueling growth in emerging markets.

- Growing push towards subscription-based smart-home services – offering managed security, remote monitoring, maintenance, and cloud-based automation enabling recurring revenue models and broader consumer reach.

Challenges & Cost Pressures

- High upfront costs and installation complexity: Despite falling device prices, comprehensive smart-home solutions still require investment in hardware, installation, connectivity and configuration a barrier in price-sensitive markets.

- Interoperability and standards fragmentation: Different devices, platforms and communication protocols often lack seamless integration, deterring users from investing in multi-device ecosystems.

- Privacy and data-security concerns: Smart-home devices collect personal data (video, usage, occupancy, energy consumption), raising consumer hesitancy unless robust security and privacy safeguards are ensured.

- Inconsistent internet connectivity and smart-infrastructure limitations: Adoption in emerging regions is constrained by patchy broadband, unstable power supply, and lack of supporting infrastructure.

- Regulatory and compliance uncertainty: Varied regional regulations around data privacy, energy efficiency, wireless communication standards, and imports/customs can hamper smooth scaling of smart-home products across borders.

Case Study: Upscaling Comfort & Efficiency in a Smart Apartment Block

A leading urban condominium developer in Southeast Asia recently partnered with a smart-home solutions provider to equip a 200-unit apartment complex with a turnkey smart-home system including smart lighting, HVAC control, security cameras, access controls, and app-based remote control. Within six months of deployment:

- Average energy consumption per unit dropped by ~20%

- Residents reported a 35% rise in satisfaction for convenience and comfort (remote temperature/light control, automated scheduling)

- Security-related incidents reduced by more than 40% (thanks to real-time monitoring and automated alerts)

- The developer gained a competitive differentiation, attracting premium tenants at 12–15% higher rents

This real-world example underscores how smart-home deployment delivers tangible value for both residents and developers combining cost savings, enhanced security and better living standards.

combined with superior switching performance")

{kind=link}